Decomposing Series

The trend extraction methods covered in the other vignettes return a

single smooth component. Often, though, an economic series is more

naturally described as the sum of three parts: a slow-moving

trend, a repeating seasonal pattern,

and an irregular remainder.

decompose_series() splits a series into these three

components and adds them as columns to the original data frame.

The theme below is used throughout the vignette for consistent styling.

library(ggplot2)

theme_series <- theme_minimal(paper = "#fefefe") +

theme(

legend.position = "bottom",

panel.grid.minor = element_blank(),

strip.background = element_rect(fill = "#2c3e50"),

strip.text = element_text(color = "#fefefe"),

axis.ticks.x = element_line(color = "gray40", linewidth = 0.5),

axis.line.x = element_line(color = "gray40", linewidth = 0.5),

axis.title.x = element_blank(),

palette.colour.discrete = c(

"#2c3e50",

"#e74c3c",

"#f39c12",

"#1abc9c",

"#9b59b6"

)

)Trend extraction vs decomposition

It is worth being clear about the difference between this function

and augment_trends().

-

augment_trends()returns only the trend (trend_*columns). The seasonal and irregular movements are simply smoothed away. -

decompose_series()returns all three components (trend_*,seasonal_*, andremainder_*), and they add back up exactly to the original series.

Because there is a seasonal component,

decompose_series() requires seasonal data: monthly

(frequency = 12) or quarterly (frequency = 4).

For annual series there is nothing seasonal to isolate, so use

augment_trends() instead.

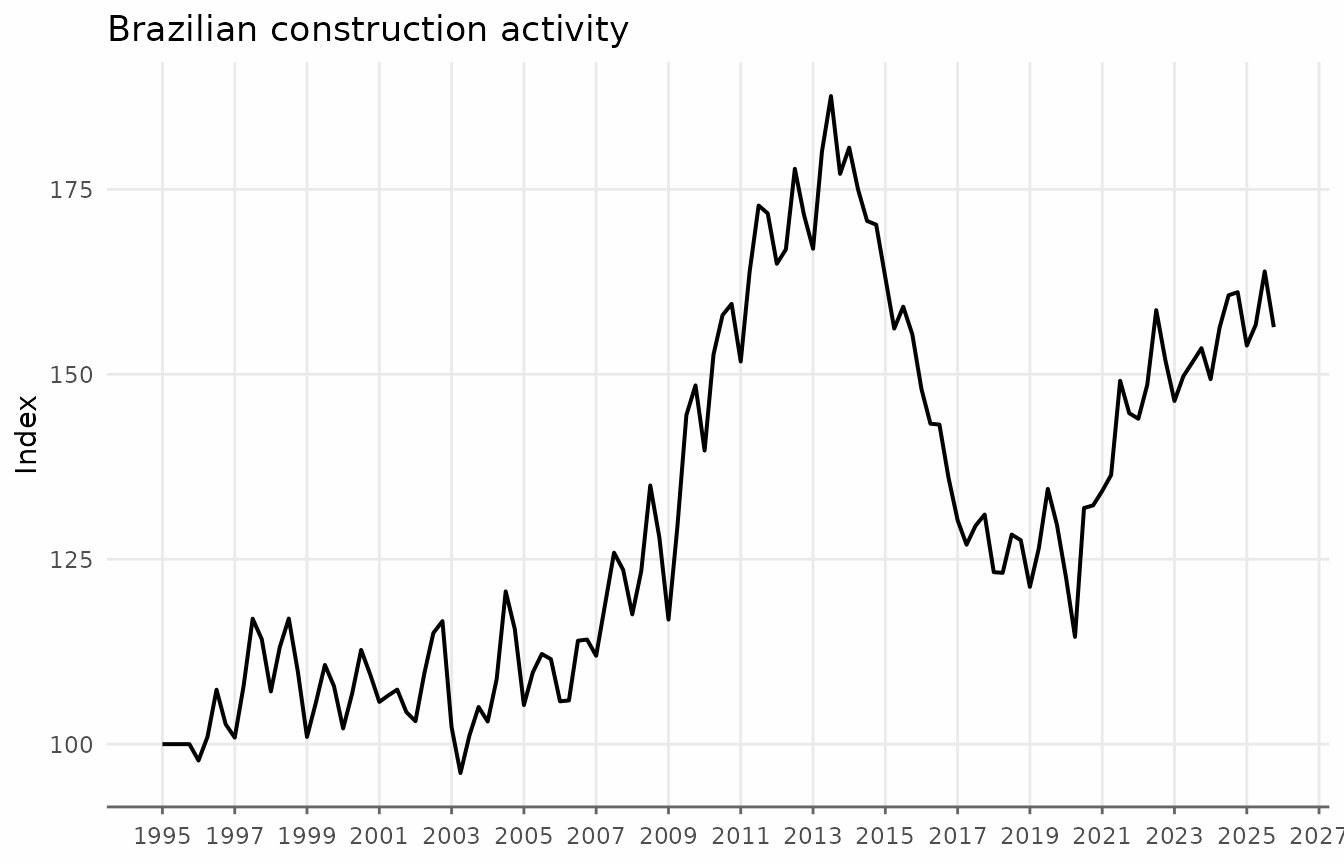

A first decomposition

Let’s start with the gdp_construction dataset, a

quarterly index of Brazilian construction activity that ships with

trendseries.

ggplot(gdp_construction, aes(date, index)) +

geom_line(lwd = 0.7) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "Brazilian construction activity",

y = "Index"

) +

theme_series

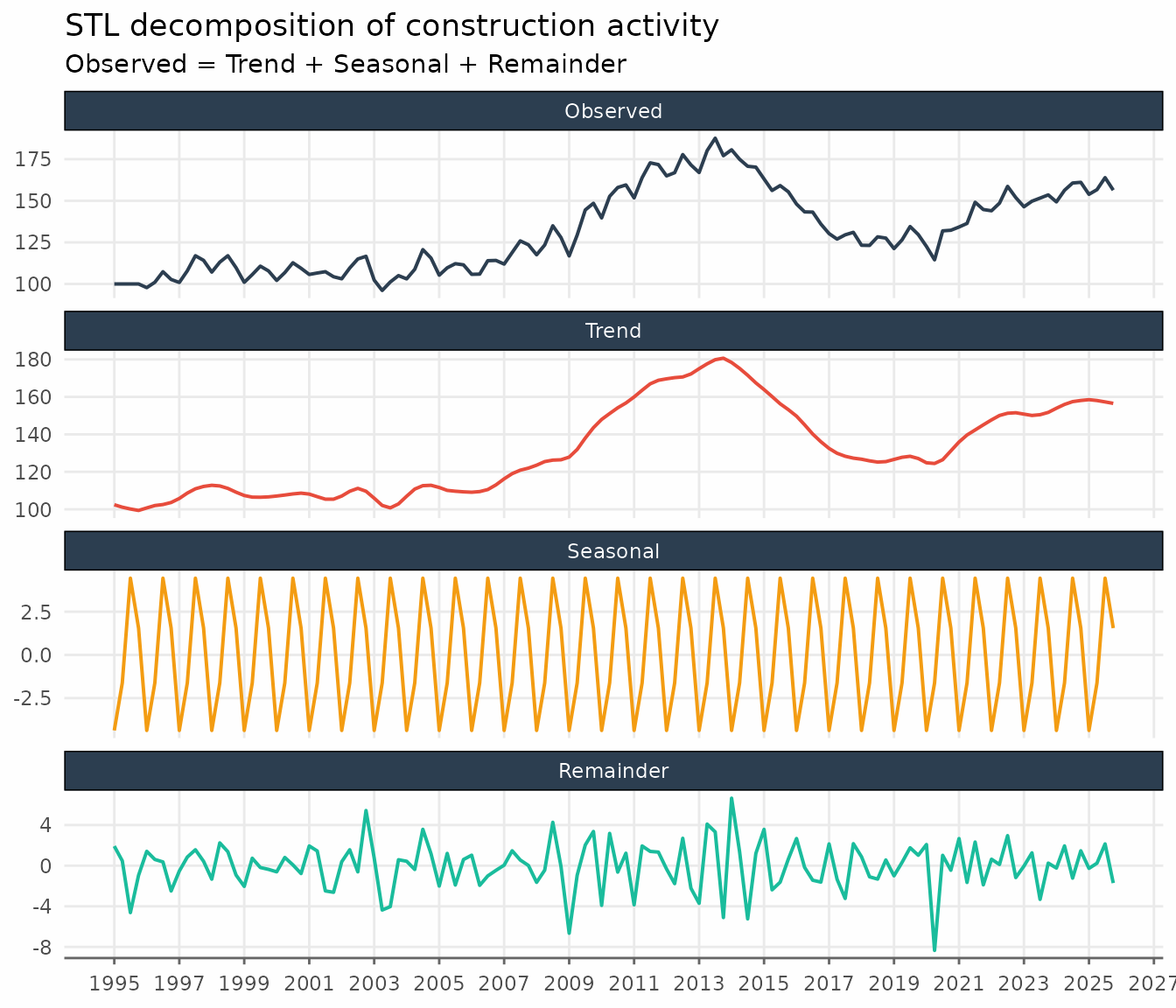

Passing the data to decompose_series() adds three new

columns. The frequency is detected automatically from the date

column.

gdp_parts <- gdp_construction |>

decompose_series(value_col = "index")

gdp_parts

#> # A tibble: 124 × 5

#> date index trend_stl seasonal_stl remainder_stl

#> <date> <dbl> <dbl> <dbl> <dbl>

#> 1 1995-01-01 100 102. -4.37 1.93

#> 2 1995-04-01 100 101. -1.62 0.476

#> 3 1995-07-01 100 100. 4.44 -4.62

#> 4 1995-10-01 100 99.4 1.55 -0.946

#> 5 1996-01-01 97.8 101. -4.37 1.42

#> 6 1996-04-01 101. 102. -1.62 0.613

#> 7 1996-07-01 107. 103. 4.44 0.370

#> 8 1996-10-01 103. 104. 1.55 -2.49

#> 9 1997-01-01 101. 106. -4.37 -0.530

#> 10 1997-04-01 108. 109. -1.62 0.849

#> # ℹ 114 more rowsThe three components are named after the method (stl by

default): trend_stl, seasonal_stl, and

remainder_stl.

Reshaping to long format makes it easy to plot the original series alongside its three components.

gdp_long <- gdp_parts |>

pivot_longer(

cols = c(index, trend_stl, seasonal_stl, remainder_stl),

names_to = "component",

values_to = "value"

) |>

mutate(

component = factor(

component,

levels = c("index", "trend_stl", "seasonal_stl", "remainder_stl"),

labels = c("Observed", "Trend", "Seasonal", "Remainder")

)

)

ggplot(gdp_long, aes(date, value)) +

geom_line(aes(color = component), lwd = 0.7, show.legend = FALSE) +

facet_wrap(vars(component), ncol = 1, scales = "free_y") +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "STL decomposition of construction activity",

subtitle = "Observed = Trend + Seasonal + Remainder",

y = NULL

) +

theme_series

STL decomposition

The default method is STL (Seasonal-Trend

decomposition via Loess), implemented with stats::stl().

The seasonal component is estimated with a loess smoother, the trend

with an adaptive moving average, and the remainder is whatever is left

over. The defaults (s.window = "periodic",

robust = FALSE) suit most economic series with a stable

seasonal pattern.

Fine control is available through the params list. The

two most useful options are an evolving seasonal pattern and robust

fitting.

# Allow the seasonal pattern to evolve slowly over time, and downweight outliers

gdp_robust <- gdp_construction |>

decompose_series(

value_col = "index",

params = list(s.window = 13, robust = TRUE)

)A s.window of "periodic" forces an

identical seasonal shape in every year; supplying a positive odd integer

instead lets that shape drift gradually. Setting

robust = TRUE reduces the influence of one-off spikes on

the trend and seasonal estimates.

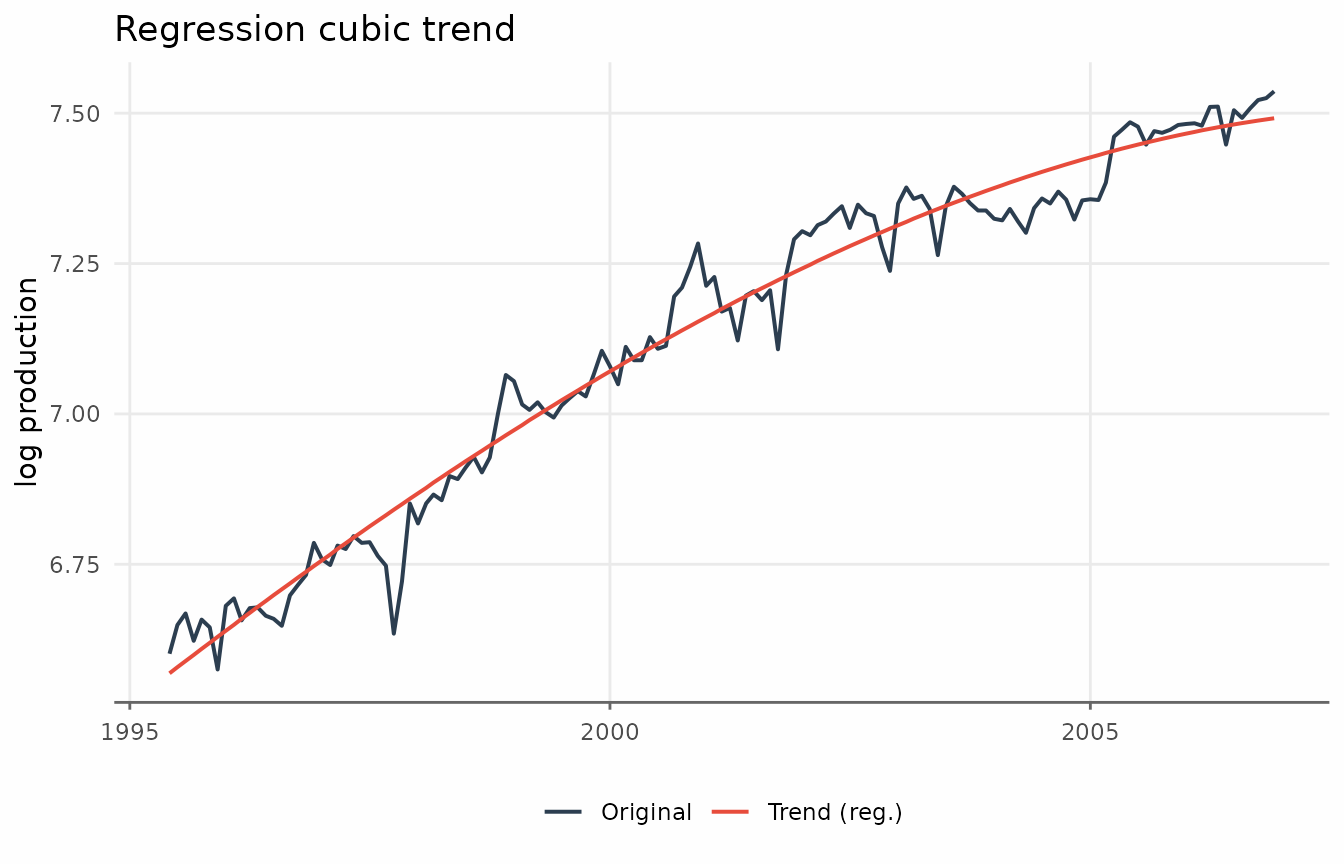

Regression decomposition

The regression method

(methods = "regression") fits a single OLS model

where is a polynomial in time and is a set of period (month or quarter) dummy variables. The trend is the constant plus the polynomial terms, the seasonal component is the period effect (centred to mean zero), and the remainder is the model residual.

Unlike STL, the regression trend is a smooth global polynomial, which

can be a better description of a series with a steady long-run

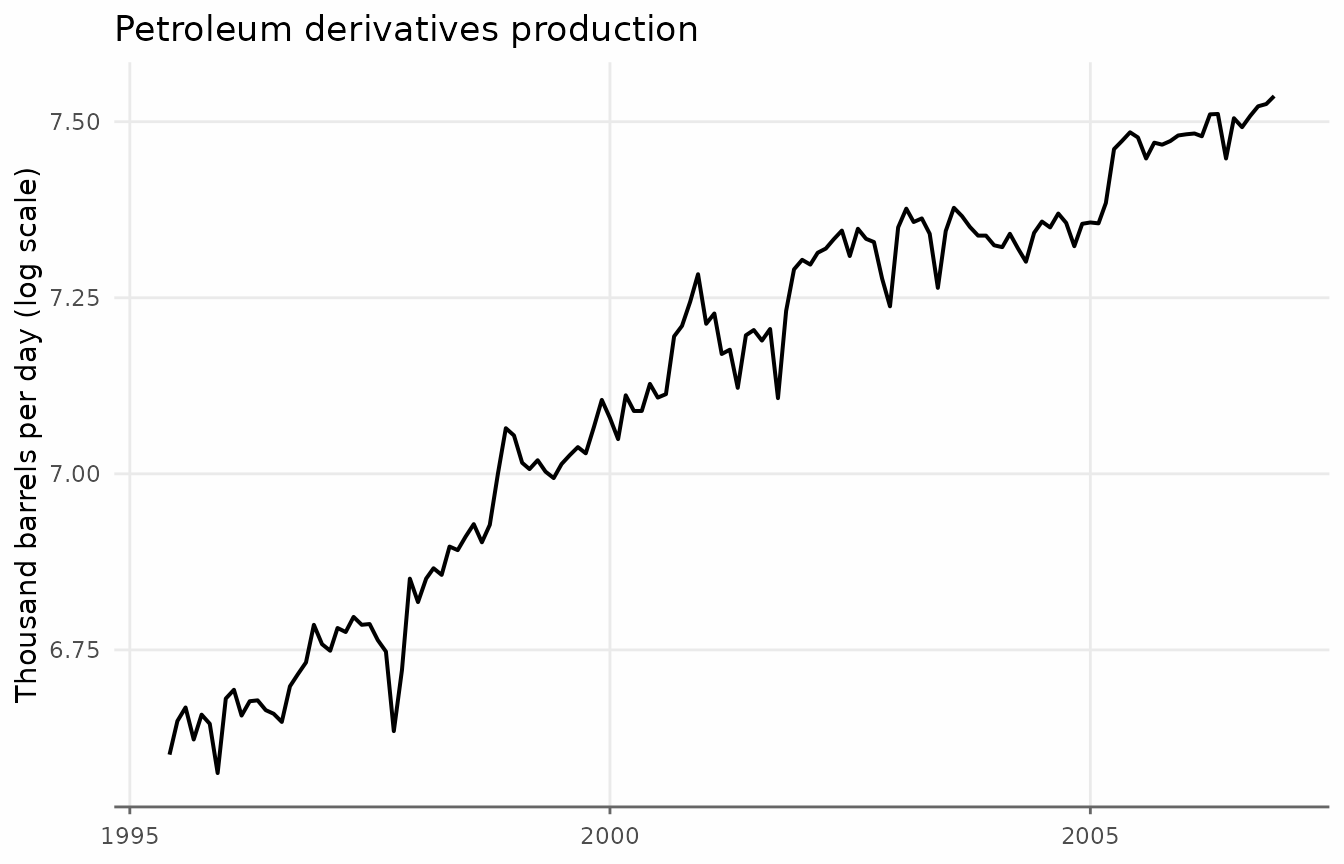

direction. For the examples that follow we use the

oil_derivatives dataset, which records monthly

petroleum-derivatives production in Brazil; we restrict it to the

1995–2006 window and work on the log scale.

suboil <- oil_derivatives |>

filter(between(date, as.Date("1995-06-01"), as.Date("2006-12-01"))) |>

mutate(lprod = log(production))

ggplot(suboil, aes(date, lprod)) +

geom_line(lwd = 0.7) +

labs(

title = "Petroleum derivatives production",

y = "Thousand barrels per day (log scale)"

) +

theme_series

The trend argument selects the polynomial form:

"linear" (the default), "quadratic", or

"cubic". Orthogonal polynomials are used by default for

numerical stability.

suboil_reg <- suboil |>

decompose_series(

value_col = "lprod",

methods = "regression",

trend = "cubic"

)

ggplot(suboil_reg, aes(date)) +

geom_line(aes(y = lprod, color = "Original"), lwd = 0.7) +

geom_line(aes(y = trend_regression, color = "Trend (reg.)"), lwd = 0.7) +

labs(title = "Regression cubic trend", y = "log production", color = NULL) +

theme_series

If the series is trend-stationary, remainder_regression

— the series with the trend and seasonality removed — is approximately

stationary.

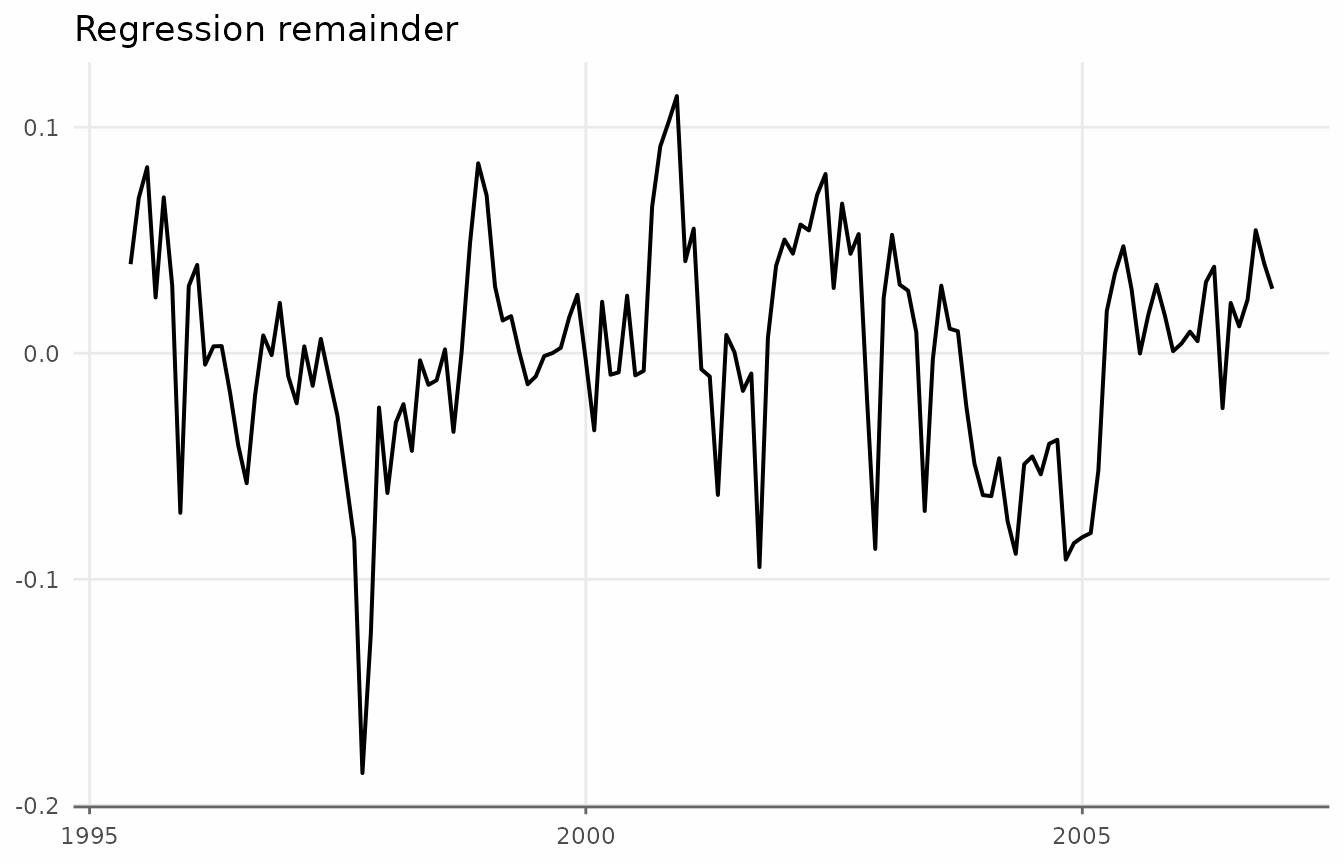

ggplot(suboil_reg, aes(date, remainder_regression)) +

geom_line(lwd = 0.7) +

labs(title = "Regression remainder", y = NULL) +

theme_series

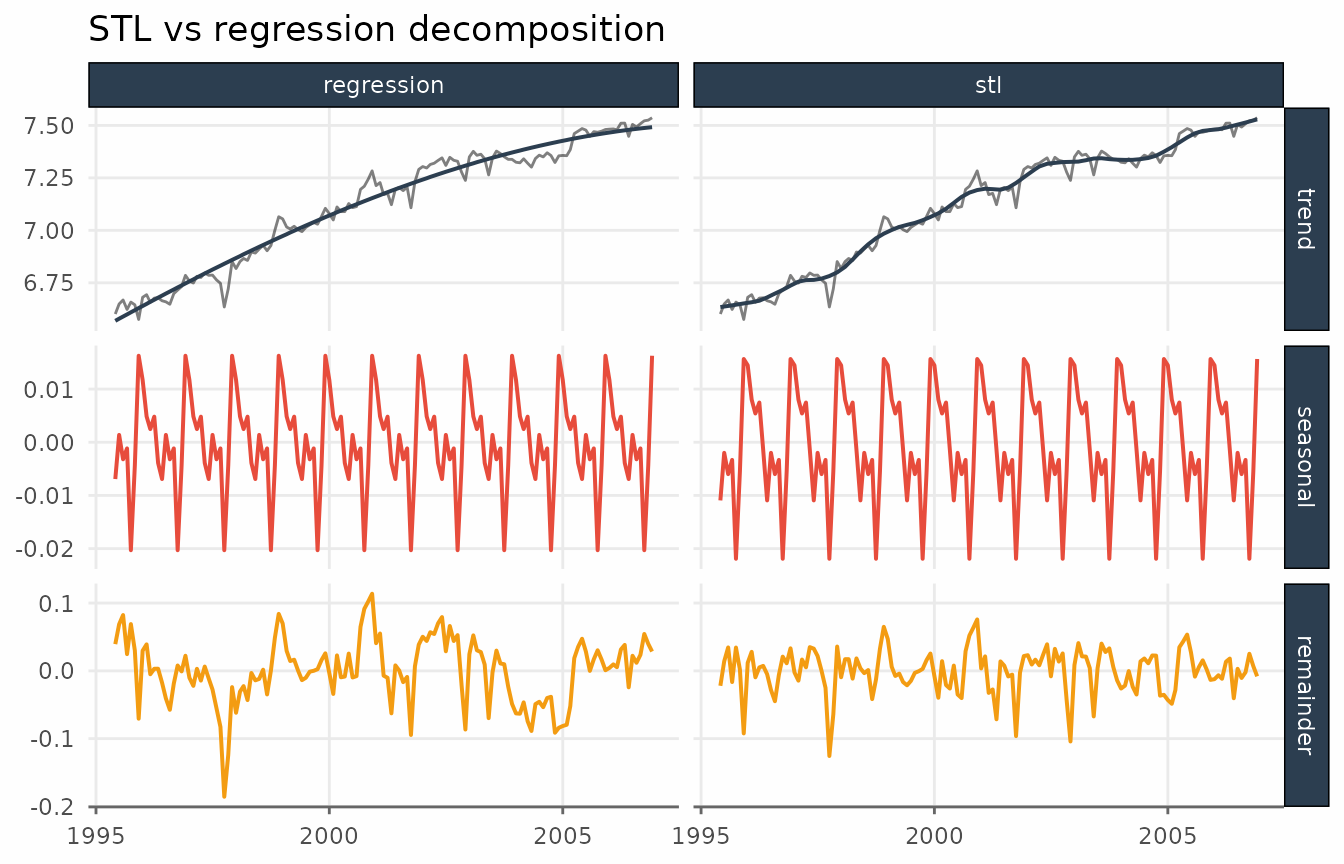

It is instructive to compare the two decomposition methods directly. Both produce fixed seasonal patterns, but STL follows short-term fluctuations more closely, producing a “cleaner” remainder.

comparison <- suboil |>

decompose_series(value_col = "lprod", methods = "stl") |>

decompose_series(value_col = "lprod", methods = "regression", trend = "cubic")

comparison_long <- comparison |>

pivot_longer(

cols = trend_stl:remainder_regression,

names_pattern = "(.*)_(.*)",

names_to = c("component", "method"),

values_to = "trend"

) |>

mutate(

component = factor(component, levels = c("trend", "seasonal", "remainder"))

)

ggplot(comparison_long, aes(date, trend)) +

# Original series

geom_line(

data = suboil,

aes(y = lprod),

layout = c(1, 2),

lwd = 0.5,

alpha = 0.5

) +

# Components and methods

geom_line(aes(y = trend, color = component), lwd = 0.7) +

facet_grid(vars(component), vars(method), scales = "free_y") +

guides(color = "none") +

labs(title = "STL vs regression decomposition", y = NULL) +

theme_series

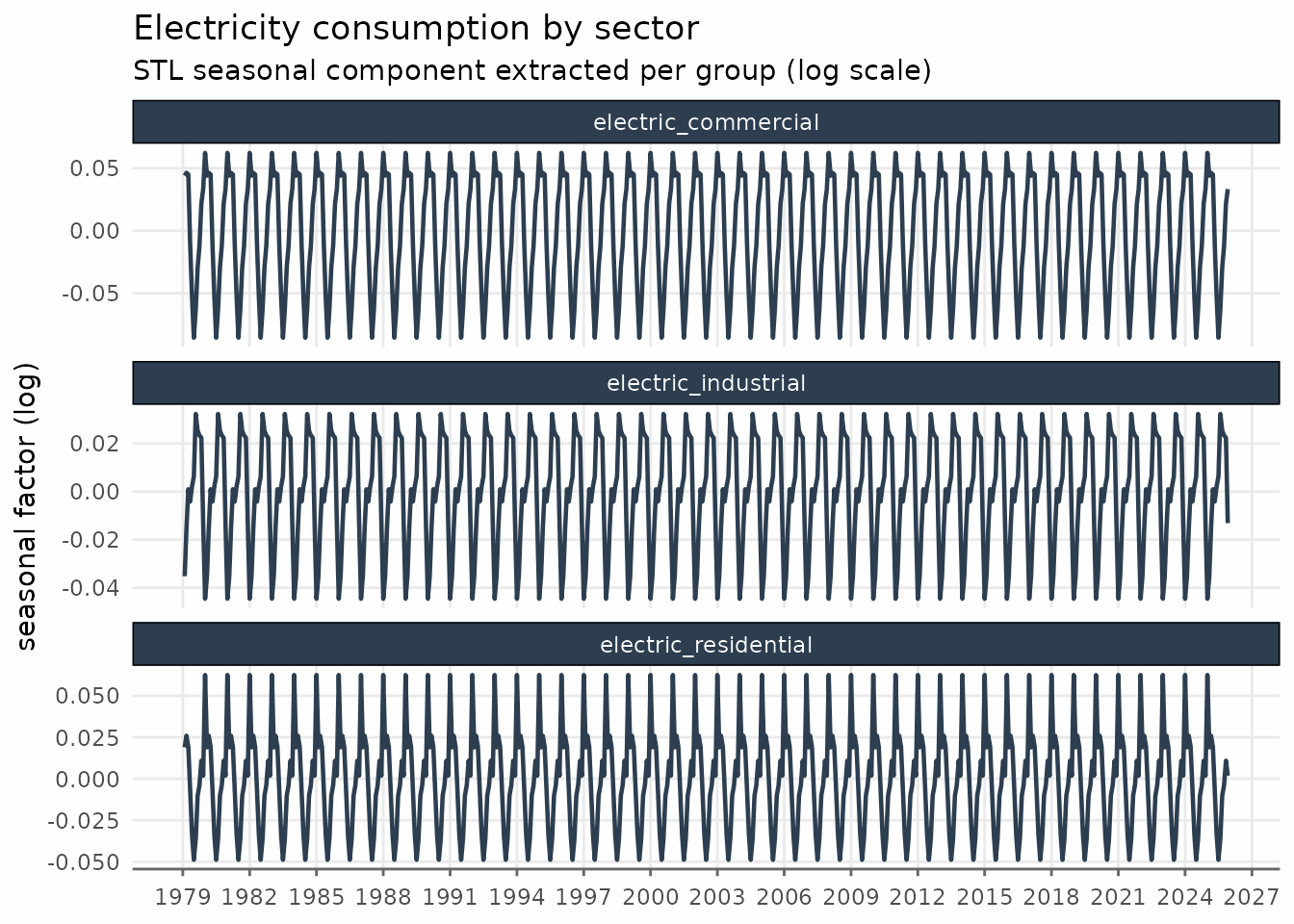

Grouped decomposition

Like augment_trends(), decompose_series()

accepts a group_cols argument to decompose several series

at once. The data must be in tidy format. Here we use the

electricity dataset, which records monthly electricity

consumption for three sectors (residential, commercial, and

industrial).

electricity_parts <- electricity |>

mutate(lvalue = log(value)) |>

decompose_series(value_col = "lvalue", group_cols = "name_series")

glimpse(electricity_parts)

#> Rows: 1,689

#> Columns: 7

#> $ date <date> 1979-02-01, 1979-03-01, 1979-04-01, 1979-05-01, 1979-06…

#> $ name_series <chr> "electric_commercial", "electric_commercial", "electric_…

#> $ value <dbl> 1030, 1057, 1044, 1038, 1002, 979, 985, 1047, 1067, 1113…

#> $ lvalue <dbl> 6.937314, 6.963190, 6.950815, 6.945051, 6.909753, 6.8865…

#> $ trend_stl <dbl> 6.908726, 6.918239, 6.927753, 6.937020, 6.946288, 6.9554…

#> $ seasonal_stl <dbl> 0.04401996, 0.04635439, 0.04502582, -0.01022254, -0.0527…

#> $ remainder_stl <dbl> -0.015431723, -0.001403624, -0.021963659, 0.018253335, 0…Each group is decomposed independently, and the components are stacked back into a single data frame.

ggplot(electricity_parts, aes(date)) +

geom_line(aes(y = seasonal_stl), color = "#2c3e50", lwd = 0.8) +

facet_wrap(vars(name_series), ncol = 1, scales = "free_y") +

scale_x_date(date_breaks = "3 years", date_labels = "%Y") +

labs(

title = "Electricity consumption by sector",

subtitle = "STL seasonal component extracted per group (log scale)",

y = "seasonal factor (log)"

) +

theme_series

Multiplicative seasonality

So far we have handled multiplicative seasonality by logging the

series before decomposing (lprod = log(production),

lvalue = log(value)). Many macroeconomic series behave this

way: the seasonal variations grow with the level of the series, so an

additive decomposition of the raw data would leave a seasonal pattern

that widens over time.

Every decompose_series() method is additive by

construction. Instead of logging manually, you can pass

transform = "log", which logs the series, decomposes it

additively, and exponentiates the components back to the original

scale.

decompose_series(

oil_derivatives,

value_col = "production",

transform = "log"

)On the log scale the additive identity holds; after exponentiating,

the components satisfy the multiplicative identity

trend * seasonal * remainder = value. Note that this

requires strictly positive data.

Other methods

Classical decomposition

methods = "classic" is the textbook decomposition

implemented by stats::decompose(). The trend is a centred

moving average of order equal to the frequency, the seasonal component

is the average detrended value for each period, and the remainder is

what is left. It is simple and fast, but shouldn’t be used in

practice.

decompose_series(

oil_derivatives,

value_col = "production",

methods = "classic",

transform = "log"

)Basic structural model

methods = "bsm" fits a Basic Structural (state-space)

Model with stats::StructTS(): stochastic level, slope, and

seasonal components estimated by maximum likelihood and extracted with

the Kalman smoother. Unlike the moving-average methods, it returns trend

and seasonal estimates for every observation and lets both

components evolve over time. The trade-off is that it relies on

numerical optimisation, which can occasionally fail to converge on short

or irregular series.

decompose_series(

suboil,

value_col = "lprod",

methods = "bsm"

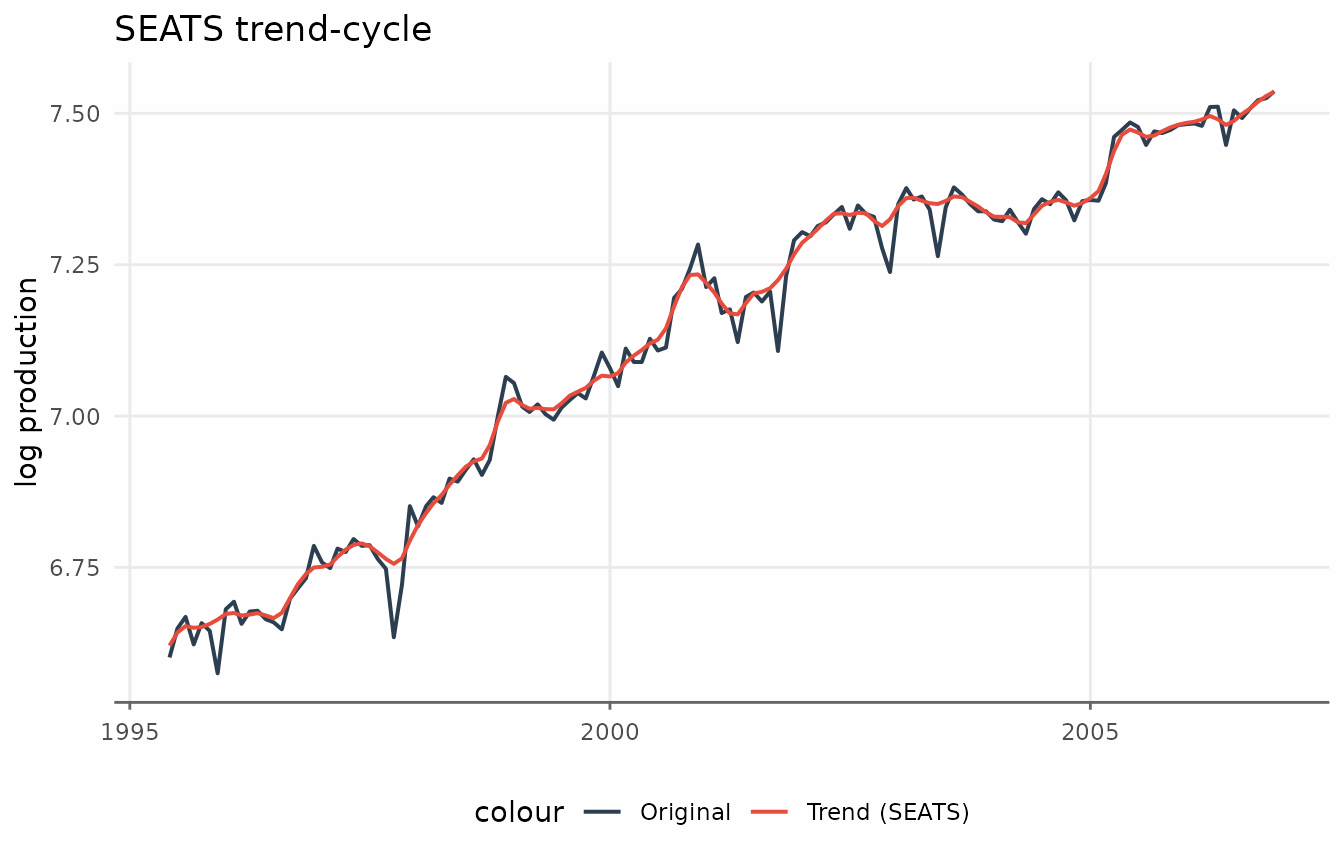

)X-13ARIMA-SEATS (seasonal)

methods = "seats" runs the U.S. Census Bureau’s

X-13ARIMA-SEATS program through the seasonal package — the

seasonal-adjustment procedure used by many statistical agencies.

seas() is called with its automatic defaults: ARIMA model

selection, log/level transformation, outlier detection, and calendar

adjustment. The SEATS trend-cycle and seasonally adjusted series are

then mapped to a trend/seasonal/remainder triple that reproduces the

original series exactly. Because X-13 selects its own transformation

internally, there is normally no need to set

transform = "log" for this method.

# requires the 'seasonal' package

seas_oil <- decompose_series(

suboil,

value_col = "lprod",

methods = "seats"

)

ggplot(seas_oil, aes(date)) +

geom_line(aes(y = lprod, color = "Original"), lwd = 0.7) +

geom_line(aes(y = trend_seats, color = "Trend (SEATS)"), lwd = 0.7) +

labs(title = "SEATS trend-cycle", y = "log production", color = NULL) +

theme_series

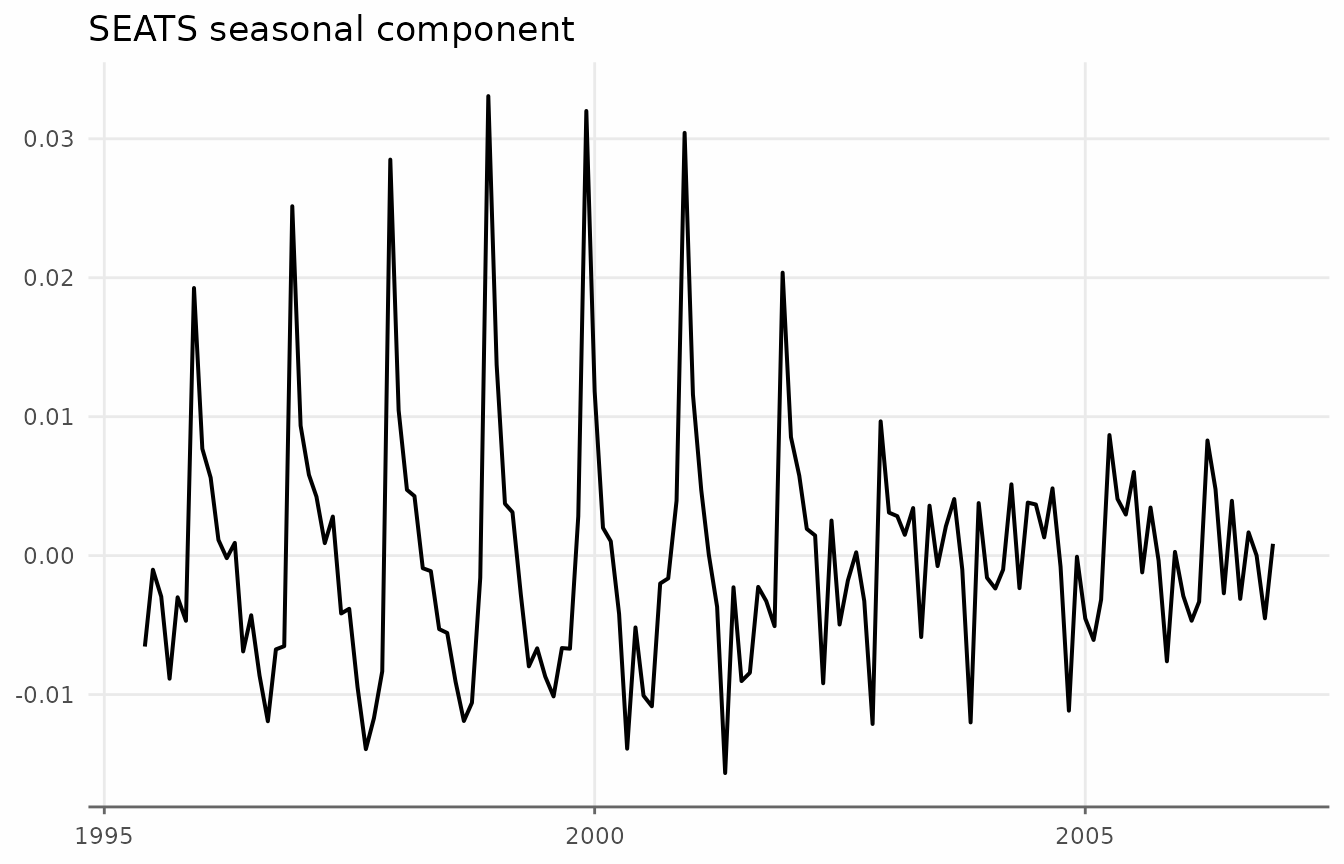

ggplot(seas_oil, aes(date, seasonal_seats)) +

geom_line(lwd = 0.7) +

labs(title = "SEATS seasonal component", y = NULL) +

theme_series

Often our interest is mainly in the series without its

seasonal component. For convenience, deseason_series()

wraps decompose_series() and returns the seasonally

adjusted series directly.

deseas_oil <- deseason_series(

suboil,

value_col = "lprod",

methods = "seats",

# set to TRUE to also return the trend, seasonal, and remainder components

components = FALSE

)

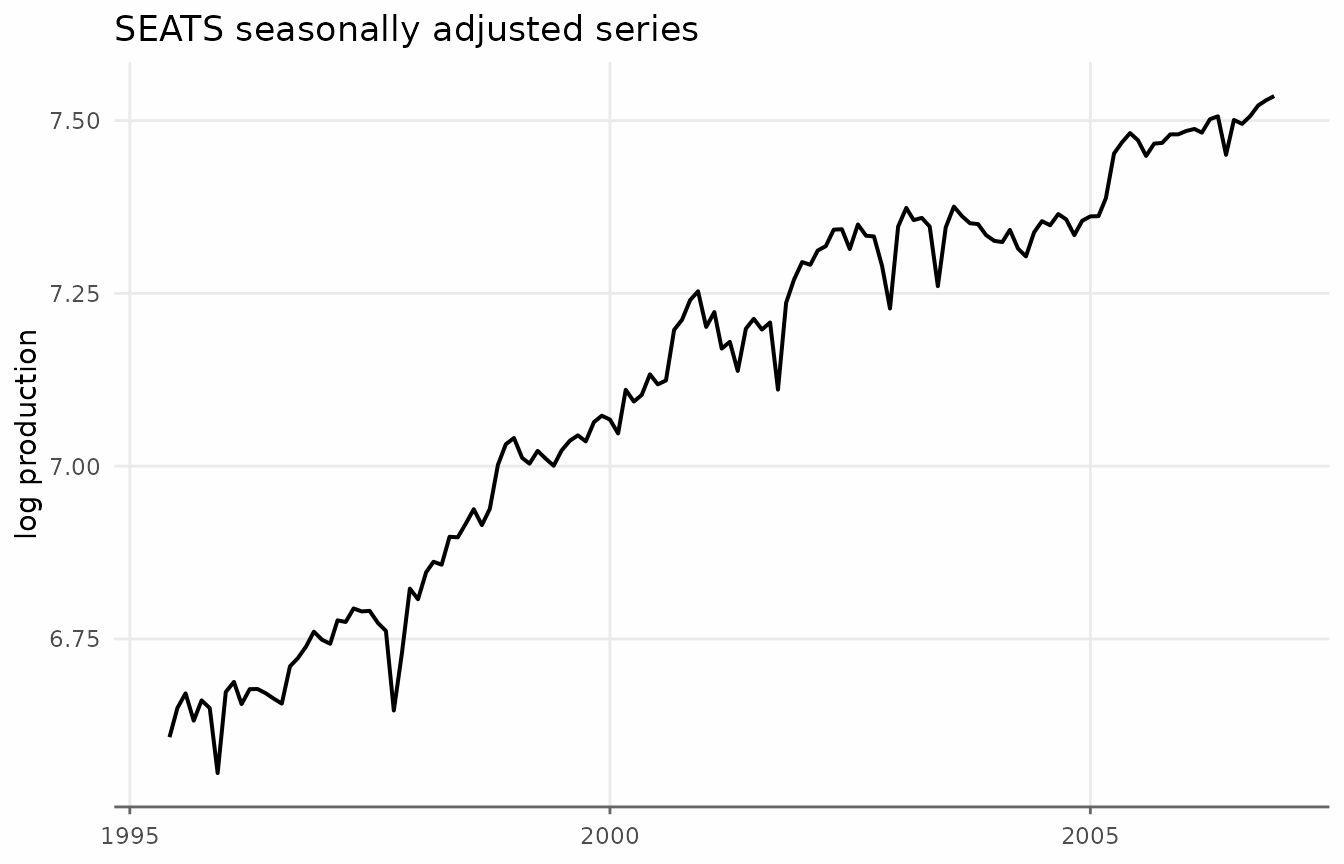

ggplot(deseas_oil, aes(date, seasadj_seats)) +

geom_line(lwd = 0.7) +

labs(

title = "SEATS seasonally adjusted series",

y = "log production"

) +

theme_series

This is equivalent to using seasadj = TRUE in

decompose_series().

decompose_series(

suboil,

value_col = "lprod",

methods = "seats",

seasadj = TRUE

)Summary

-

decompose_series()splits a seasonal (monthly or quarterly) series into trend, seasonal, and remainder components that sum to the original series. - There are five available methods:

"stl"(default),"regression","classic","bsm", and"seats" - All methods are additive; use

transform = "log"for multiplicative seasonality, where the components instead multiply to the original series. -

deseason_series()is a convenience wrapper that returns only the seasonally adjusted series.