trendseries provides a unified interface to extract trends, cycles, and seasonal components from time series. Most filtering methods in R are designed for ts objects, but datasets typically come in a data.frame format with a date column, which makes applying filters cumbersome. trendseries bridges this gap: augment_trends(), decompose_series(), deseason_series(), and detrend_series() all work directly on data.frame/tibble objects, while extract_trends() provides the same methods for ts/xts/zoo objects when you need to stay in native time-series format.

Installation

trendseries is available on CRAN

install.packages("trendseries")You can install the development version of trendseries from GitHub.

# install.packages("remotes")

remotes::install_github("viniciusoike/trendseries")Main Functions

The package provides four main functions for data.frame/tibble/data.table workflows:

-

augment_trends(): adds trend columns to the original dataset. -

decompose_series(): splits a series into trend, seasonal, and remainder components. -

deseason_series(): wrapsdecompose_series()to return a seasonally adjusted series. -

detrend_series(): wrapsaugment_trends()to return the deviation from trend (the cycle).

Each has a ts/xts/zoo-native counterpart via extract_trends(), for workflows that stay in native time-series format.

Usage

Time series have a specific structure in R (ts) and most filtering methods are designed for ts objects. However, datasets typically come in a data.frame format with a date column, which can make applying filters cumbersome.

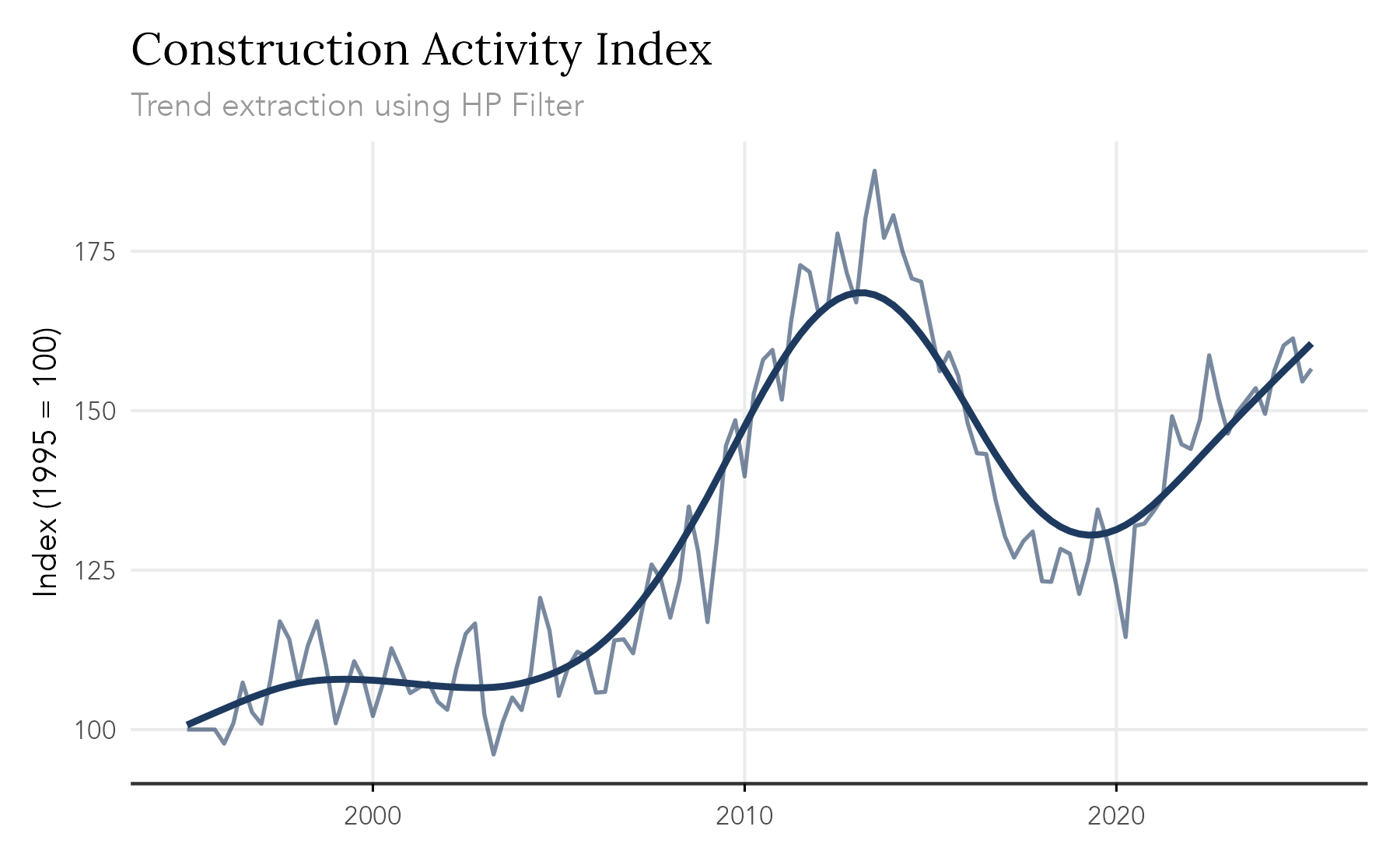

trendseries aims to make this process easy and flexible. The example below computes three filters (HP, STL, and moving average) on a quarterly index of construction activity. Note that the augment_trends() function automatically detects the frequency of the data and uses conventional defaults for the HP filter.

library(trendseries)

library(ggplot2)

data(gdp_construction)

# Computes multiple trends at once

series <- gdp_construction |>

# Automatically detects frequency

# Trends are added as new columns to the original dataset

augment_trends(

value_col = "index",

methods = c("hp", "stl", "ma")

)

#> Auto-detected quarterly (4 obs/year)

#> Computing HP filter (two-sided) with lambda = 1600

#> Computing STL trend with s.window = periodic

#> Computing 2x4-period MA (auto-adjusted for even-window centering)

series

#> # A tibble: 124 × 5

#> date index trend_hp trend_stl trend_ma

#> <date> <dbl> <dbl> <dbl> <dbl>

#> 1 1995-01-01 100 101. 102. NA

#> 2 1995-04-01 100 101. 101. 99.7

#> 3 1995-07-01 100 102. 100. 99.6

#> 4 1995-10-01 100 103. 99.4 101.

#> 5 1996-01-01 97.8 103. 101. 102.

#> 6 1996-04-01 101. 104. 102. 103.

#> 7 1996-07-01 107. 104. 103. 104.

#> 8 1996-10-01 103. 105. 104. 106.

#> 9 1997-01-01 101. 106. 106. 109.

#> 10 1997-04-01 108. 106. 109. 111.

#> # ℹ 114 more rows

An equivalent extract_trends() function is also available for ts objects.

stl_trend <- extract_trends(AirPassengers, methods = "stl")

#> Computing STL trend with s.window = periodic

plot.ts(AirPassengers)

lines(stl_trend, col = "#C53030")

Available Methods

trendseries supports 20 trend estimation methods, covering the most commonly used approaches in econometrics and statistics. The Trend Extraction Methods vignette describes each one — when to use it and which parameters it takes.

| Method | Category | Description |

|---|---|---|

hp |

econometric | Hodrick-Prescott filter |

hamilton |

econometric | Hamilton regression filter |

bn |

econometric | Beveridge-Nelson decomposition |

ucm |

econometric | Unobserved components model |

bk |

bandpass | Baxter-King bandpass filter |

cf |

bandpass | Christiano-Fitzgerald bandpass filter |

ma |

moving average | Simple moving average |

wma |

moving average | Weighted moving average |

ewma |

moving average | Exponentially weighted moving average |

triangular |

moving average | Triangular moving average |

median |

moving average | Median filter |

gaussian |

moving average | Gaussian-weighted moving average |

spencer |

moving average | Spencer’s 15-term moving average |

henderson |

moving average | Henderson moving average |

stl |

smoothing | Seasonal-trend decomposition via Loess |

loess |

smoothing | Local polynomial regression |

spline |

smoothing | Smoothing splines |

poly |

smoothing | Polynomial trends |

kernel |

smoothing | Kernel smoother |

kalman |

smoothing | Kalman filter/smoother |

Decomposition

To split a series into trend, seasonal, and remainder components, use decompose_series(). It supports STL, regression, classical moving-average, Basic Structural Model (BSM), and X-13ARIMA-SEATS decomposition:

gdp_construction |>

decompose_series(value_col = "index", methods = "stl")See the Decomposing Series vignette for details.