Housing credit in Brazil is organized around the SFH (Sistema Financeiro da Habitação), in which most mortgages are funded by savings deposits (SBPE) and by the FGTS workers’ fund. This article follows the credit cycle from funding to lending using three datasets

-

abecipfor savings flows and financed units, -

bcb_seriesfor lending volumes, rates, and delinquency, -

bcb_realestatefor the regional distribution of the credit stock.

The code below defines a common theme for the plots in this article. It is entirely optional and can be omitted.

color_palette <- c(

"#1E3A5F",

"#DD6B20",

"#2C7A7B",

"#D69E2E",

"#805AD5",

"#C53030"

)

theme_series <- function() {

theme_minimal(base_size = 10) +

theme(

plot.title = element_text(size = 16),

panel.grid.minor = element_blank(),

panel.grid.major.x = element_blank(),

axis.line.x = element_line(color = "gray10", linewidth = 0.5),

axis.ticks.x = element_line(color = "gray10", linewidth = 0.5),

axis.title.x = element_blank(),

legend.position = "bottom",

palette.color.discrete = color_palette

)

}Funding: savings deposits

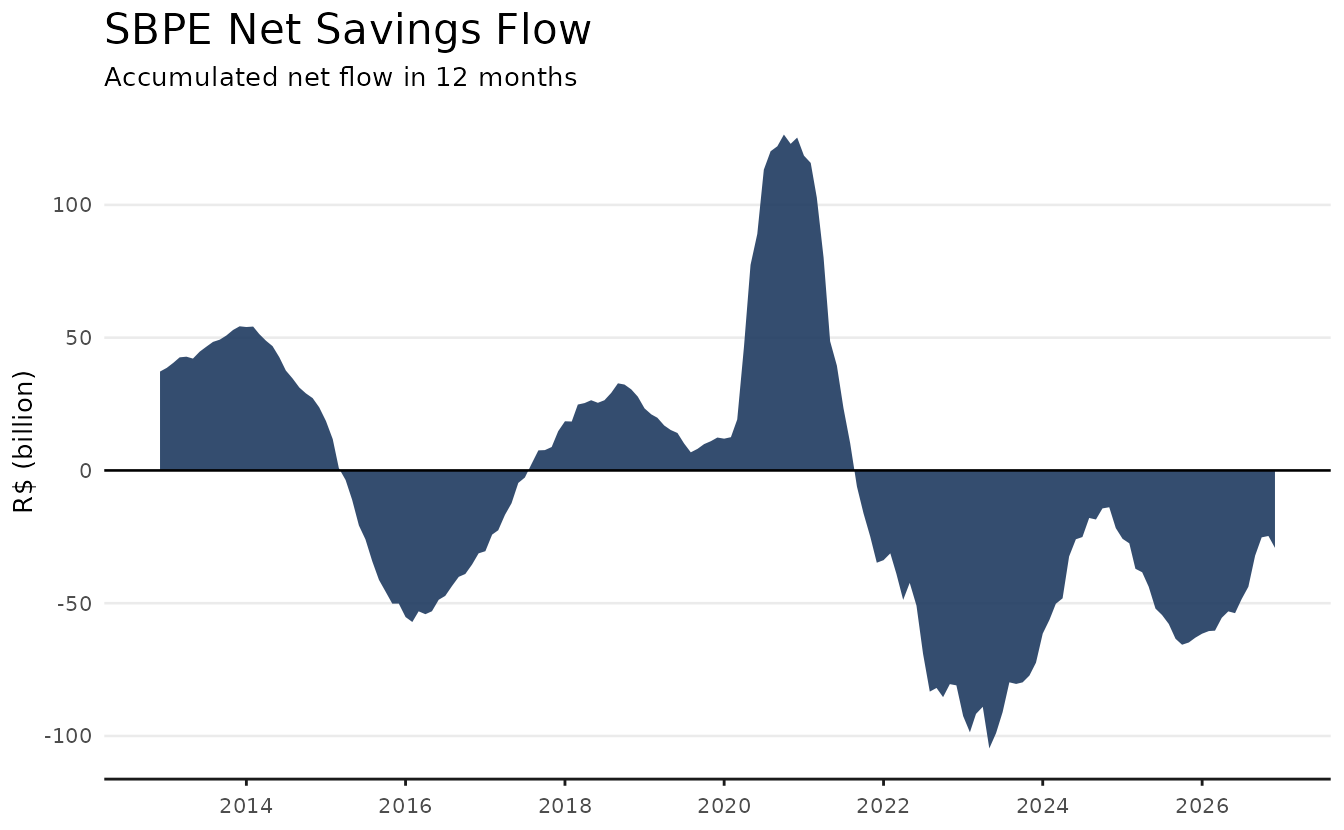

SBPE savings accounts are the cheapest funding source for mortgages,

so sustained withdrawals eventually constrain new lending. The

sbpe table from abecip tracks monthly

deposits, withdrawals, and the resulting stock.

sbpe <- get_dataset("abecip", table = "sbpe")

glimpse(sbpe)

#> Rows: 540

#> Columns: 15

#> $ date <date> 1982-01-01, 1982-02-01, 1982-03-01, 1982-04-01, 198…

#> $ sbpe_inflow <dbl> 238234.1, 224080.0, 247218.8, 264925.0, 227636.3, 31…

#> $ sbpe_outflow <dbl> 261523.1, 161176.0, 118662.8, 378395.0, 137201.3, 15…

#> $ sbpe_netflow <dbl> -23289, 62904, 128556, -113470, 90435, 164739, -9934…

#> $ sbpe_netflow_pct <dbl> -0.009387130, 0.021881448, 0.043761242, -0.037006429…

#> $ sbpe_yield <dbl> 417103, 0, 0, 485995, 0, 0, 642432, 0, 0, 957944, 0,…

#> $ sbpe_stock <dbl> 2874764, 2937668, 3066224, 3438749, 3529184, 3693923…

#> $ rural_inflow <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ rural_outflow <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ rural_netflow <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ rural_netflow_pct <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ rural_yield <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ rural_stock <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ total_stock <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …

#> $ total_netflow <dbl> NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, NA, …The plot shows the accumulated net flow over twelve months. Periods of persistent outflows, such as the years after 2021, signal tighter funding ahead.

sbpe_flows <- sbpe |>

filter(date >= as.Date("2012-01-01")) |>

mutate(

netflow_12m = zoo::rollsumr(sbpe_netflow, k = 12, fill = NA) / 1e3

)

ggplot(sbpe_flows, aes(date, netflow_12m)) +

geom_area(fill = color_palette[1], alpha = 0.9) +

geom_hline(yintercept = 0) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "SBPE Net Savings Flow",

subtitle = "Accumulated net flow in 12 months",

y = "R$ (billion)"

) +

theme_series()

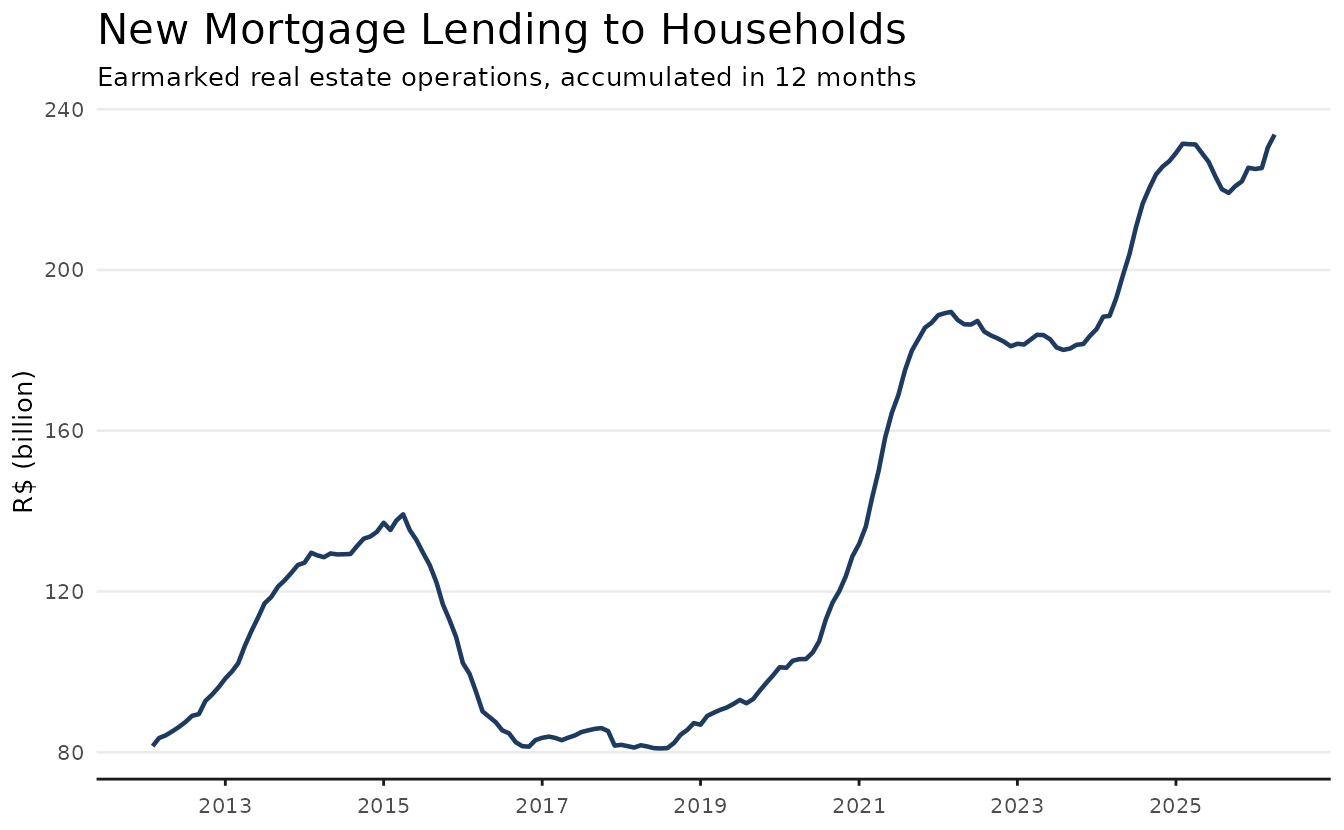

Lending: new mortgage loans

The flow of new real estate loans to households is reported by the

Central Bank. The series below is part of the core table of

bcb_series, which gathers the most relevant real estate

credit series.

bcb <- get_dataset("bcb_series", table = "core")

fimob <- bcb |>

filter(name_simplified == "fimob_pf_total") |>

mutate(

lending_12m = zoo::rollsumr(value, k = 12, fill = NA) / 1e3

)

ggplot(filter(fimob, !is.na(lending_12m)), aes(date, lending_12m)) +

geom_line(color = color_palette[1], lwd = 0.8) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "New Mortgage Lending to Households",

subtitle = "Earmarked real estate operations, accumulated in 12 months",

y = "R$ (billion)"

) +

theme_series()

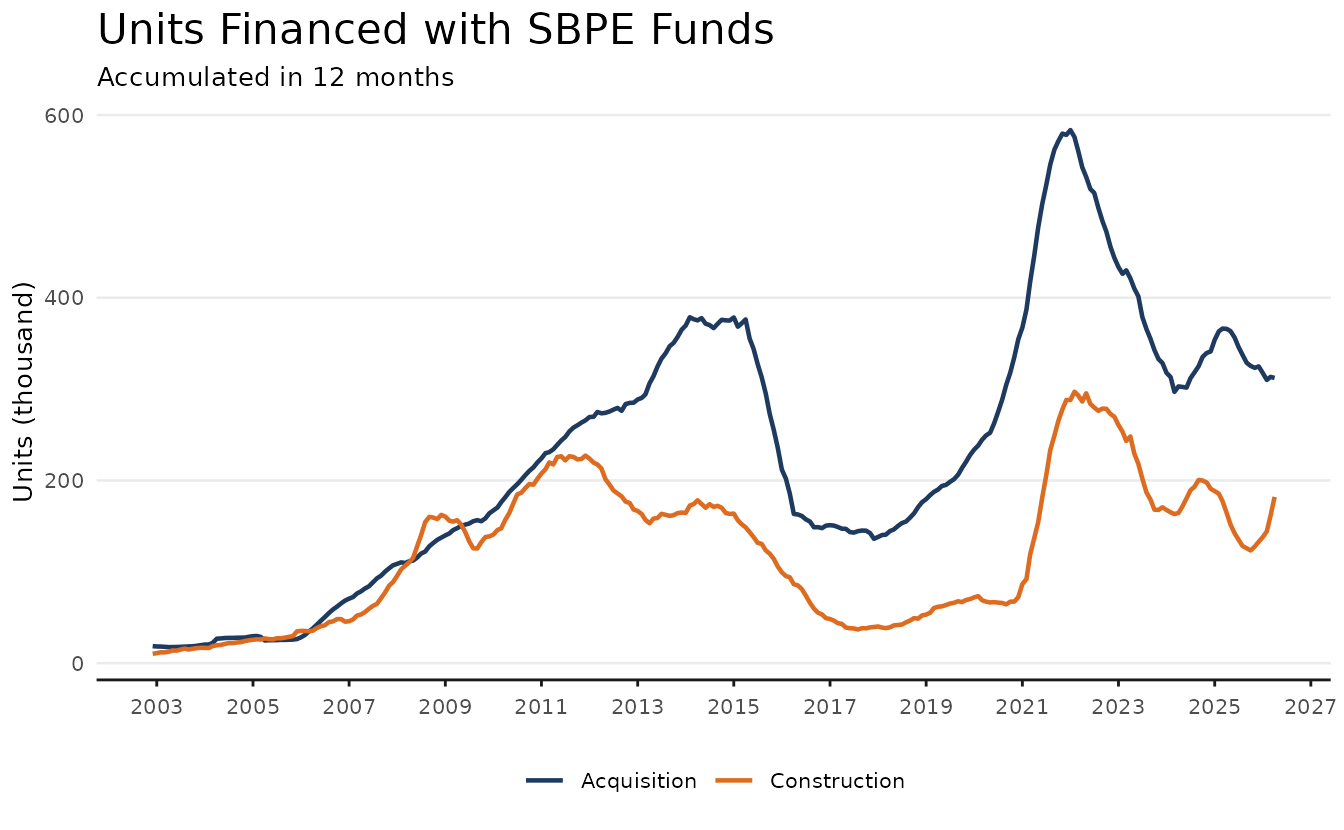

In physical terms, the units table from

abecip counts how many homes were financed with SBPE funds,

split between construction and acquisition loans.

units <- get_dataset("abecip", table = "units")

units_12m <- units |>

select(date, units_construction, units_acquisition) |>

tidyr::pivot_longer(-date, names_to = "type", values_to = "units") |>

mutate(

units_12m = zoo::rollsumr(units, k = 12, fill = NA) / 1e3,

type_label = if_else(

type == "units_construction", "Construction", "Acquisition"

),

.by = type

)

ggplot(filter(units_12m, !is.na(units_12m)), aes(date, units_12m)) +

geom_line(aes(color = type_label), lwd = 0.8) +

scale_color_manual(values = color_palette[c(1, 2)]) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "Units Financed with SBPE Funds",

subtitle = "Accumulated in 12 months",

y = "Units (thousand)",

color = NULL

) +

theme_series()

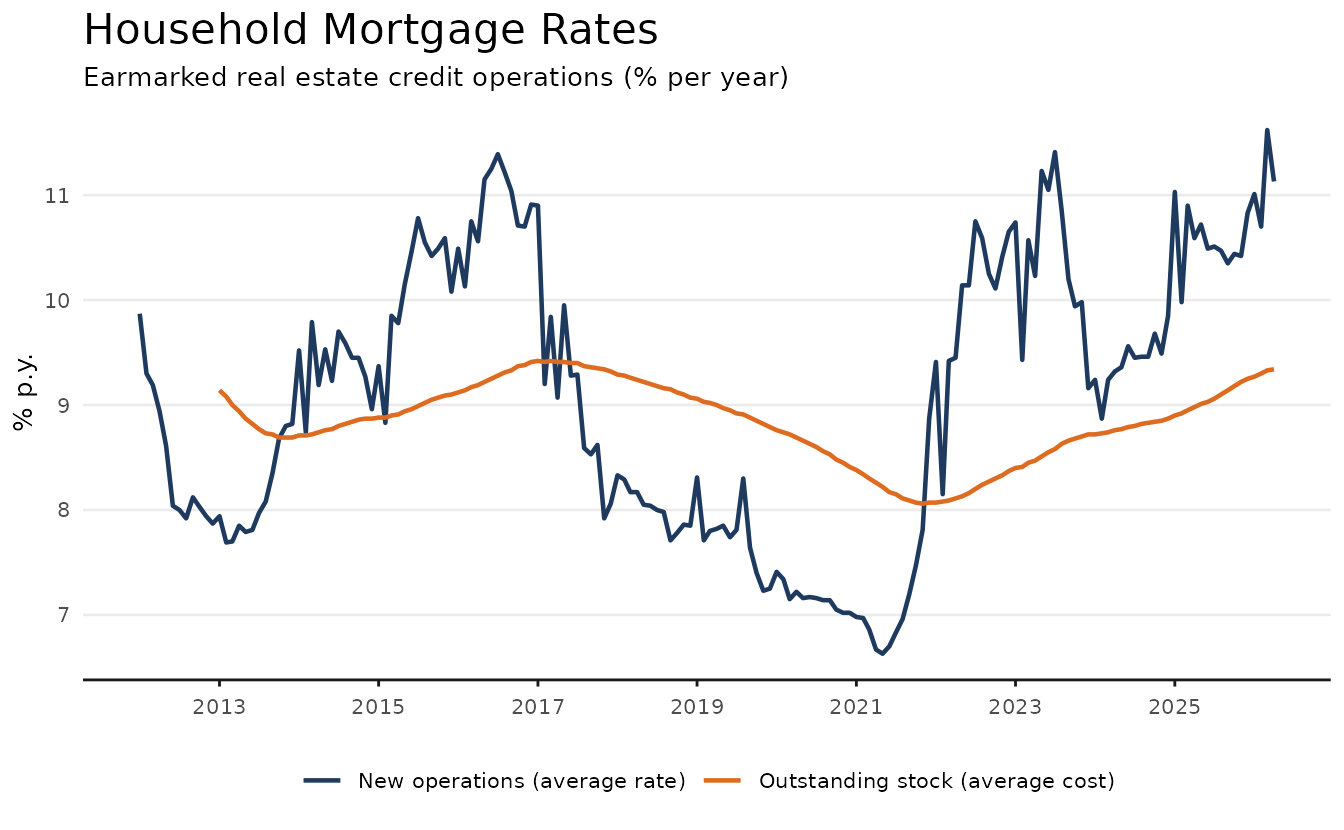

The price of credit

Mortgage rates move with monetary policy but are partly insulated by

regulated pricing within the SFH. The core table includes

both the average rate charged on new operations and the average cost of

the outstanding stock, which adjusts much more slowly.

rates <- bcb |>

filter(name_simplified %in% c("taxa_fimob_pf_total", "icc_fimob")) |>

mutate(

rate_label = if_else(

name_simplified == "icc_fimob",

"Outstanding stock (average cost)",

"New operations (average rate)"

)

)

rates_recent <- filter(rates, date >= as.Date("2012-01-01"))

ggplot(rates_recent, aes(date, value)) +

geom_line(aes(color = rate_label), lwd = 0.8) +

scale_color_manual(values = color_palette[c(1, 2)]) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "Household Mortgage Rates",

subtitle = "Earmarked real estate credit operations (% per year)",

y = "% p.y.",

color = NULL

) +

theme_series()

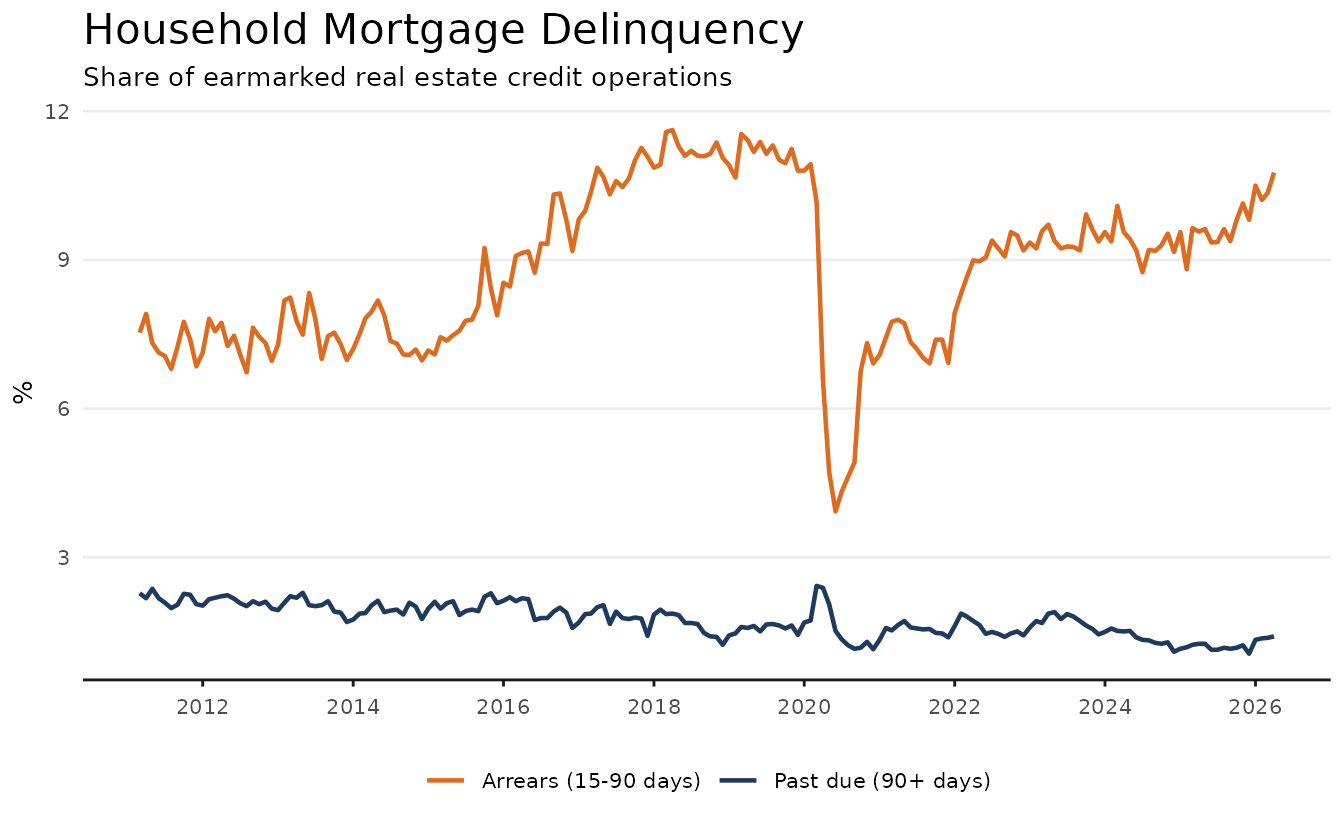

Credit risk

Delinquency in housing credit is structurally low because loans are collateralized. Even so, arrears track the economic cycle.

risk <- bcb |>

filter(

name_simplified %in% c(

"inad_credito_direcionado_pf_fimob",

"atraso_fimob_pf_total"

)

) |>

mutate(

risk_label = if_else(

name_simplified == "atraso_fimob_pf_total",

"Arrears (15-90 days)",

"Past due (90+ days)"

)

)

ggplot(risk, aes(date, value)) +

geom_line(aes(color = risk_label), lwd = 0.8) +

scale_color_manual(values = color_palette[c(2, 1)]) +

scale_x_date(date_breaks = "2 years", date_labels = "%Y") +

labs(

title = "Household Mortgage Delinquency",

subtitle = "Share of earmarked real estate credit operations",

y = "%",

color = NULL

) +

theme_series()

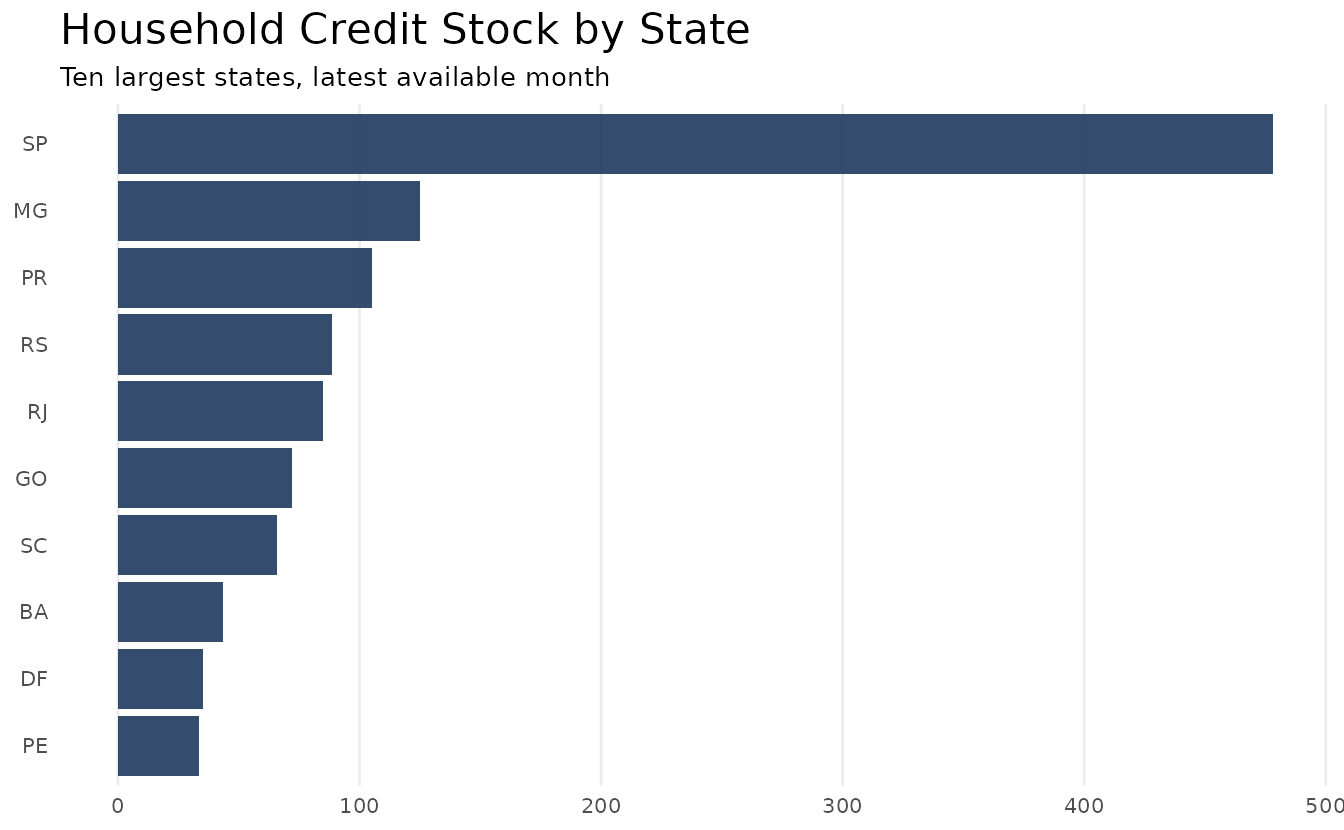

Where the credit is

The bcb_realestate dataset breaks the credit stock down

by state. The code below sums the household credit portfolio across

credit lines for the latest available month.

bcb_re <- get_dataset("bcb_realestate")

stock_states <- bcb_re |>

filter(

category == "credito",

type == "estoque",

v1 == "carteira",

v2 == "credito",

v3 == "pf",

abbrev_state != "BR",

date == max(date)

) |>

summarise(stock = sum(value) / 1e9, .by = abbrev_state) |>

slice_max(stock, n = 10)

ggplot(stock_states, aes(reorder(abbrev_state, stock), stock)) +

geom_col(fill = color_palette[1], alpha = 0.9) +

coord_flip() +

labs(

title = "Household Credit Stock by State",

subtitle = "Ten largest states, latest available month",

x = NULL,

y = "R$ (billion)"

) +

theme_series() +

theme(

panel.grid.major.x = element_line(),

panel.grid.major.y = element_blank(),

axis.line.x = element_blank(),

axis.ticks.x = element_blank()

)

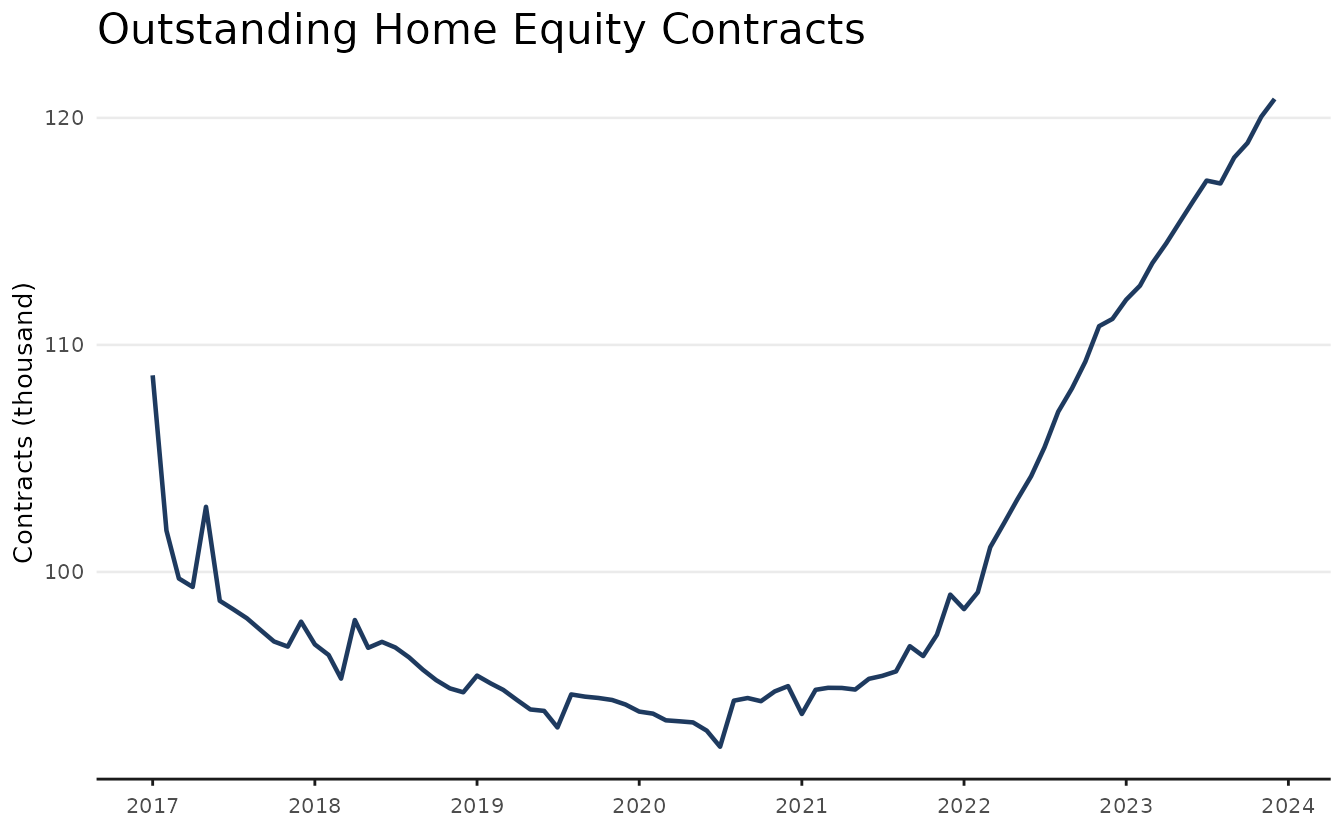

Home equity lending

Home equity loans (CGI, Crédito com Garantia de Imóvel) remain a

small but growing market. The cgi table from

abecip summarizes contracts, balances, and default

rates.

cgi <- get_dataset("abecip", table = "cgi")

glimpse(cgi)

#> Rows: 84

#> Columns: 8

#> $ year <dbl> 2017, 2017, 2017, 2017, 2017, 2017, 2017, 2017, 20…

#> $ date <date> 2017-01-01, 2017-02-01, 2017-03-01, 2017-04-01, 2…

#> $ new_contracts <dbl> 1323, 1197, 1324, 809, 926, 982, 928, 905, 781, 80…

#> $ stock_contracts <dbl> 108661, 101825, 99712, 99340, 102869, 98730, 98359…

#> $ loan <dbl> 181295778, 157080758, 195053012, 132217320, 174307…

#> $ outstanding_balance <dbl> 12725110368, 11120992240, 10598834209, 10514921327…

#> $ average_term <dbl> 144.8, 145.3, 140.8, 130.2, 134.3, 128.7, 137.4, 1…

#> $ default_rate <dbl> 4.8, 5.0, 4.9, 5.2, 4.7, 4.4, 5.0, 4.7, 4.6, 4.7, …

ggplot(cgi, aes(date, stock_contracts / 1e3)) +

geom_line(color = color_palette[1], lwd = 0.8) +

scale_x_date(date_breaks = "1 year", date_labels = "%Y") +

labs(

title = "Outstanding Home Equity Contracts",

y = "Contracts (thousand)"

) +

theme_series()

Learn more

The column-level documentation of each dataset used here is available

in the help topics ?abecip, ?bcb_series, and

?bcb_realestate. For price indices, see the vignette

vignette("working-with-rppi").