library(trendseries)

library(dplyr)

library(ggplot2)

library(tidyr)

# Load data

data("electric", "vehicles", "ibcbr", package = "trendseries")Introduction

This vignette covers advanced trend extraction methods that go beyond simple moving averages and standard economic filters. These methods are designed for specific situations:

- STL decomposition: Seasonal data with complex patterns

- Kalman filter: Optimal smoothing with state-space models

- Savitzky-Golay filter: Preserving peaks and local features

- Spline smoothing: Highly flexible nonparametric trends

- LOESS: Locally adaptive smoothing

STL Decomposition: Handling Seasonality

STL (Seasonal-Trend decomposition using LOESS) is ideal for data with regular seasonal patterns. It decomposes a time series into three components: seasonal, trend, and remainder.

Basic STL Example

Let’s use electricity consumption data, which has clear seasonal patterns:

# Get recent electricity data

electric_recent <- electric |>

slice_tail(n = 72) # Last 6 years

# Apply STL decomposition

electric_stl <- electric_recent |>

augment_trends(

value_col = "electric",

methods = "stl"

)

# STL returns the trend component

head(electric_stl)

#> # A tibble: 6 × 3

#> date electric trend_stl

#> <date> <dbl> <dbl>

#> 1 2019-08-01 10987 11709.

#> 2 2019-09-01 11379 11759.

#> 3 2019-10-01 11973 11810.

#> 4 2019-11-01 12424 11865.

#> 5 2019-12-01 12201 11921.

#> 6 2020-01-01 12909 11981.Visualize the decomposition:

# Calculate seasonal and remainder components

electric_decomp <- electric_stl |>

mutate(

seasonal = electric - trend_stl, # Approximate seasonal (for visualization)

trend = trend_stl

)

# Plot original and trend

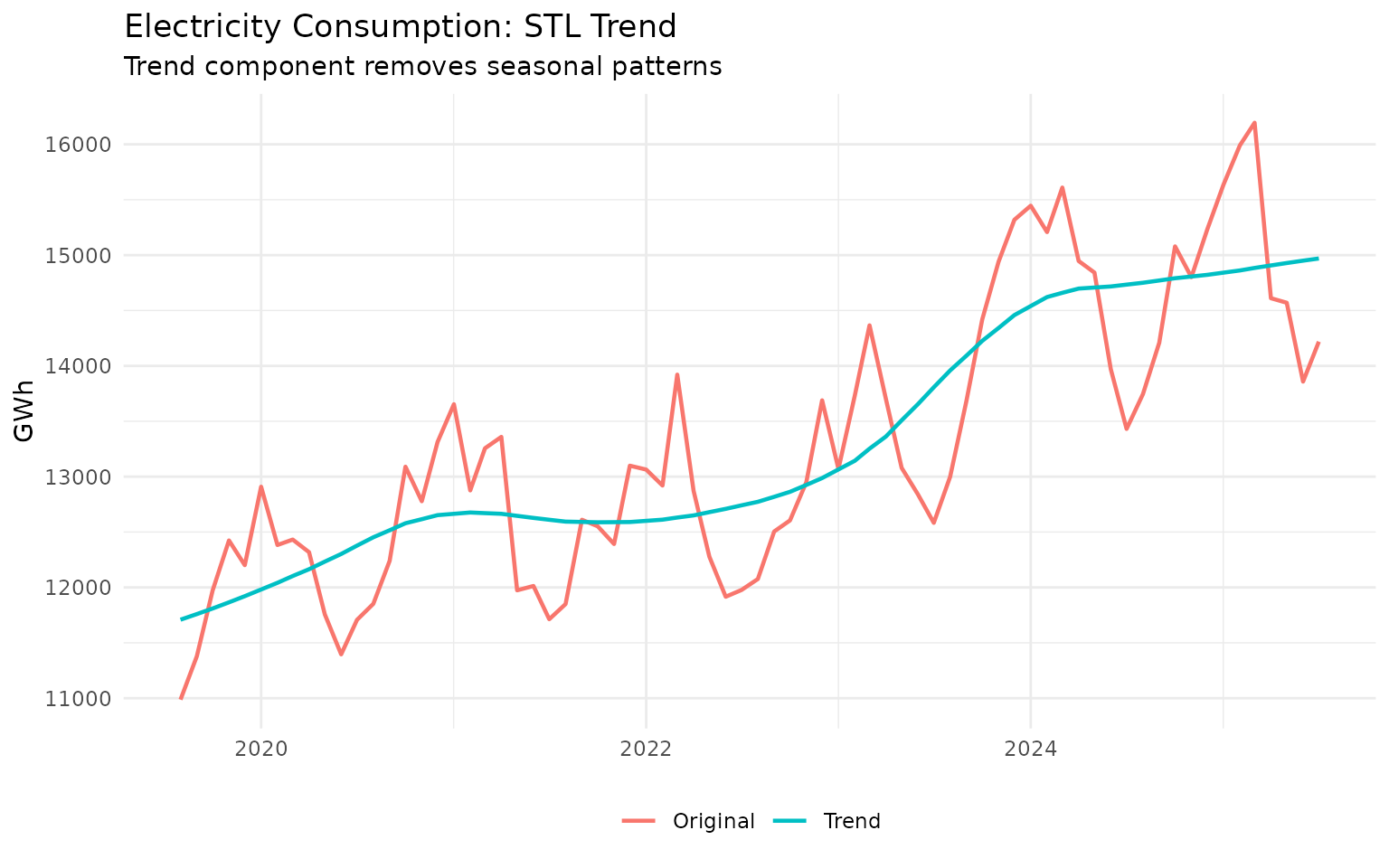

p1 <- electric_decomp |>

select(date, electric, trend) |>

pivot_longer(cols = c(electric, trend), names_to = "series") |>

mutate(series = ifelse(series == "electric", "Original", "Trend")) |>

ggplot(aes(x = date, y = value, color = series)) +

geom_line(linewidth = 0.8) +

labs(

title = "Electricity Consumption: STL Trend",

subtitle = "Trend component removes seasonal patterns",

x = NULL,

y = "GWh",

color = NULL

) +

theme_minimal() +

theme(legend.position = "bottom")

print(p1)

Notice how the STL trend is much smoother than the original data because it has removed the seasonal fluctuations.

Comparing STL with HP Filter on Seasonal Data

Let’s compare STL with the HP filter on the same seasonal data:

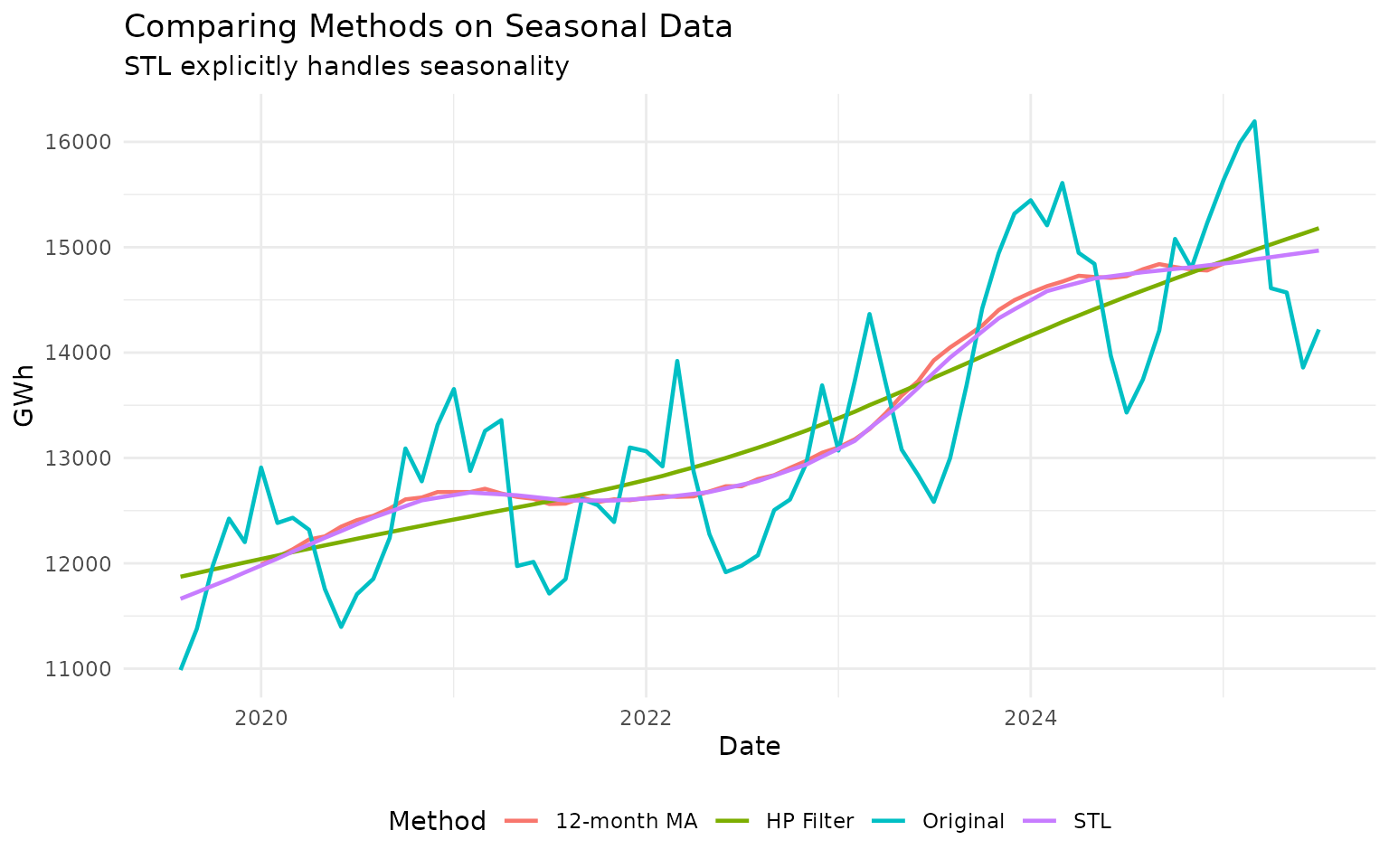

# Apply both methods

electric_comparison <- electric_recent |>

augment_trends(

value_col = "electric",

methods = c("stl", "hp", "ma"),

window = 12 # 12-month window for MA

)

# Plot comparison

electric_comparison |>

select(date, electric, trend_stl, trend_hp, trend_ma) |>

pivot_longer(

cols = c(electric, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "electric" ~ "Original",

method == "trend_stl" ~ "STL",

method == "trend_hp" ~ "HP Filter",

method == "trend_ma" ~ "12-month MA"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Comparing Methods on Seasonal Data",

subtitle = "STL explicitly handles seasonality",

x = "Date",

y = "GWh",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

All three methods remove seasonality to some degree, but STL is specifically designed for this purpose.

When to Use STL

Use STL when: - Data has clear monthly or quarterly seasonal patterns - Seasonality strength varies over time - You want to separately analyze seasonal and trend components

Don’t use STL when: - Data has no seasonality (use HP or MA instead) - Seasonal pattern is irregular (try other methods) - You have very short time series (need at least 2 full cycles)

Kalman Filter: Optimal Statistical Smoothing

The Kalman filter provides statistically optimal smoothing under certain assumptions. It’s based on state-space models and is widely used in engineering and finance.

Basic Kalman Smoothing

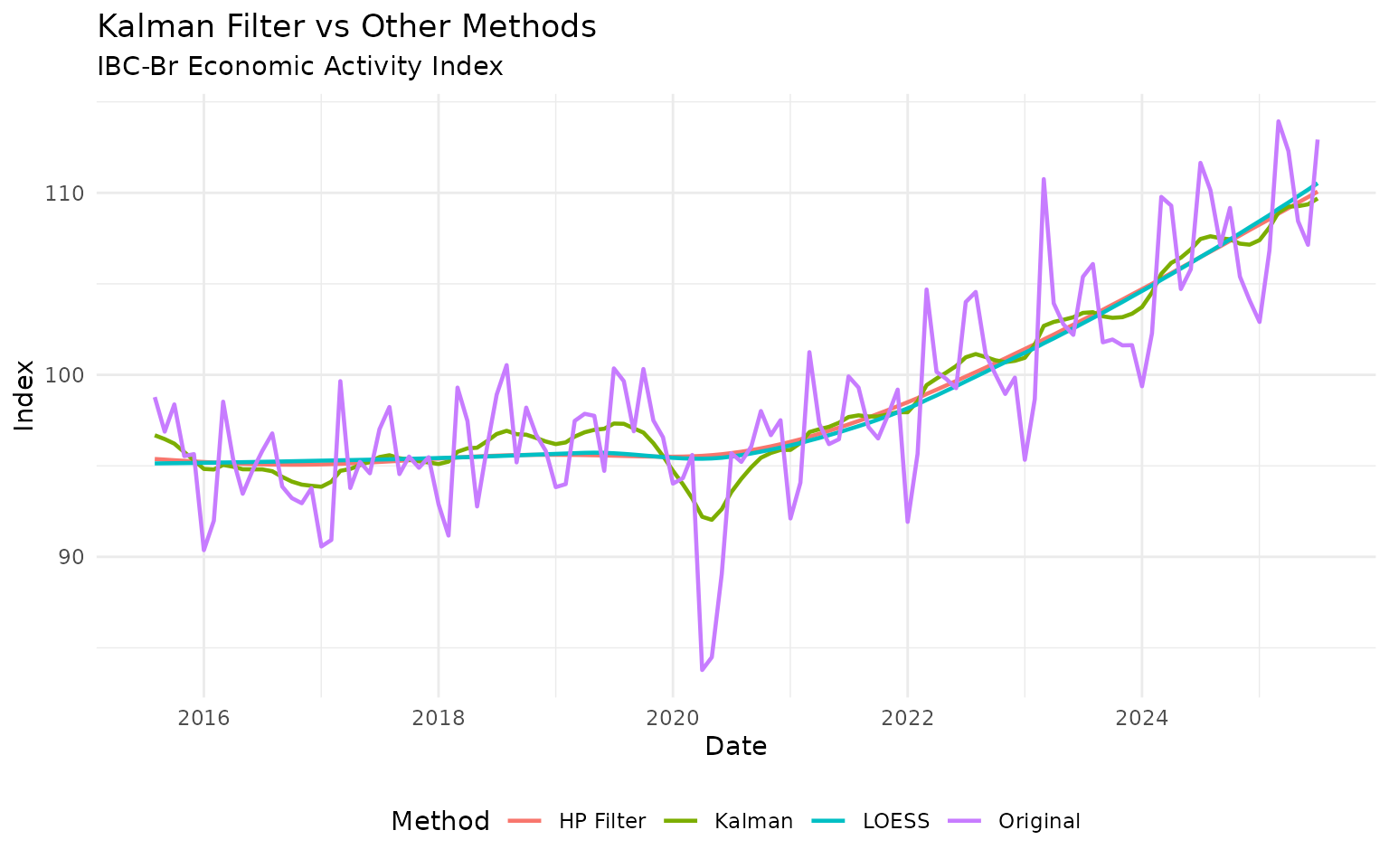

# Apply Kalman filter to IBC-Br data

ibcbr_recent <- ibcbr |>

slice_tail(n = 120)

ibcbr_kalman <- ibcbr_recent |>

augment_trends(

value_col = "ibcbr",

methods = "kalman"

)

# Compare with HP filter

ibcbr_comparison <- ibcbr_recent |>

augment_trends(

value_col = "ibcbr",

methods = c("kalman", "hp", "loess")

)

# Plot

ibcbr_comparison |>

select(date, ibcbr, starts_with("trend_")) |>

pivot_longer(

cols = c(ibcbr, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "ibcbr" ~ "Original",

method == "trend_kalman" ~ "Kalman",

method == "trend_hp" ~ "HP Filter",

method == "trend_loess" ~ "LOESS"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Kalman Filter vs Other Methods",

subtitle = "IBC-Br Economic Activity Index",

x = "Date",

y = "Index",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

Adjusting Kalman Smoothing

You can control the smoothness with the smoothing

parameter (higher values = more smoothing):

# Try different smoothing levels

smoothing_levels <- c(0.5, 1.0, 2.0, 5.0)

vehicles_recent <- vehicles |>

slice_tail(n = 60)

vehicles_kalman <- vehicles_recent

for (s in smoothing_levels) {

temp <- vehicles_recent |>

augment_trends(value_col = "vehicles", methods = "kalman", smoothing = s) |>

select(trend_kalman)

names(temp) <- paste0("kalman_", s)

vehicles_kalman <- bind_cols(vehicles_kalman, temp)

}

# Plot

vehicles_kalman |>

select(date, vehicles, starts_with("kalman_")) |>

pivot_longer(

cols = c(vehicles, starts_with("kalman_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "vehicles" ~ "Original",

method == "kalman_0.5" ~ "Light smoothing",

method == "kalman_1" ~ "Medium smoothing",

method == "kalman_2" ~ "Heavy smoothing",

method == "kalman_5" ~ "Very heavy smoothing"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Kalman Filter with Different Smoothing Levels",

subtitle = "Higher values produce smoother trends",

x = "Date",

y = "Production (thousands)",

color = NULL

) +

theme_minimal() +

theme(legend.position = "bottom")

When to use Kalman: - You want statistically principled smoothing - Data is noisy but has a clear underlying trend - You need real-time filtering (Kalman works well with streaming data)

Savitzky-Golay Filter: Preserving Features

The Savitzky-Golay (SG) filter is designed to preserve local features like peaks and valleys while smoothing. It fits local polynomials to the data.

Basic SG Example

# Apply SG filter to vehicle production

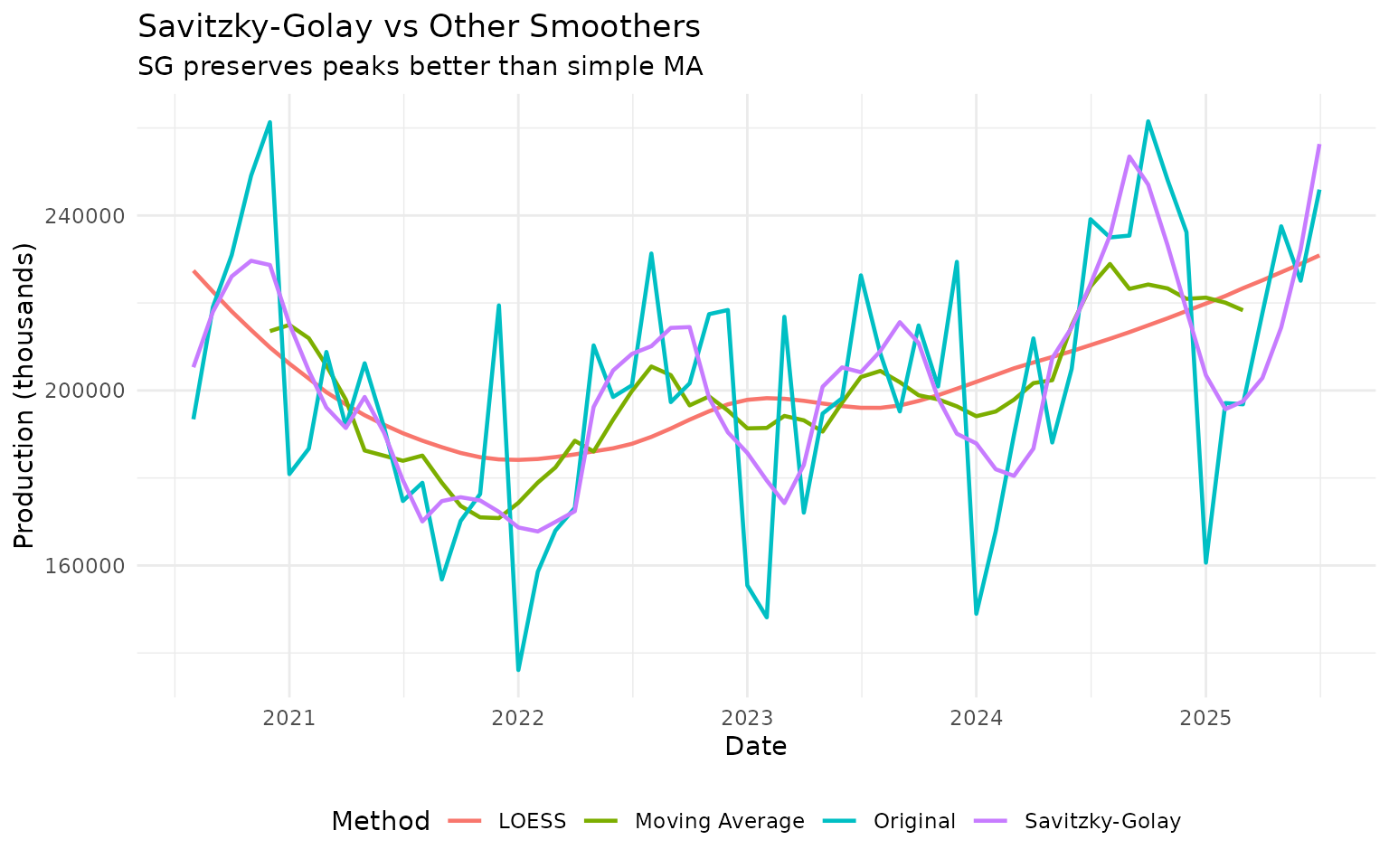

vehicles_sg <- vehicles_recent |>

augment_trends(

value_col = "vehicles",

methods = "sg",

window = 9 # Must be odd number

)

# Compare SG with MA

vehicles_comparison <- vehicles_recent |>

augment_trends(

value_col = "vehicles",

methods = c("sg", "ma", "loess"),

window = 9

)

# Plot

vehicles_comparison |>

select(date, vehicles, starts_with("trend_")) |>

pivot_longer(

cols = c(vehicles, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "vehicles" ~ "Original",

method == "trend_sg" ~ "Savitzky-Golay",

method == "trend_ma" ~ "Moving Average",

method == "trend_loess" ~ "LOESS"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Savitzky-Golay vs Other Smoothers",

subtitle = "SG preserves peaks better than simple MA",

x = "Date",

y = "Production (thousands)",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

Notice how SG preserves peaks and valleys better than the simple moving average.

Polynomial Order

You can adjust the polynomial order (higher order = more flexible):

# Try different polynomial orders

vehicles_sg_poly <- vehicles_recent |>

augment_trends(

value_col = "vehicles",

methods = "sg",

window = 9,

params = list(sg_poly_order = 2)

) |>

rename(sg_order2 = trend_sg)

vehicles_sg_poly <- vehicles_sg_poly |>

augment_trends(

value_col = "vehicles",

methods = "sg",

window = 9,

params = list(sg_poly_order = 3)

) |>

rename(sg_order3 = trend_sg)

vehicles_sg_poly <- vehicles_sg_poly |>

augment_trends(

value_col = "vehicles",

methods = "sg",

window = 9,

params = list(sg_poly_order = 4)

)

# Plot

vehicles_sg_poly |>

select(date, vehicles, sg_order2, sg_order3, trend_sg) |>

pivot_longer(

cols = c(vehicles, sg_order2, sg_order3, trend_sg),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "vehicles" ~ "Original",

method == "sg_order2" ~ "Order 2 (quadratic)",

method == "sg_order3" ~ "Order 3 (cubic)",

method == "trend_sg" ~ "Order 4"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Savitzky-Golay with Different Polynomial Orders",

subtitle = "Higher orders preserve more detail",

x = "Date",

y = "Production (thousands)",

color = NULL

) +

theme_minimal() +

theme(legend.position = "bottom")

When to use Savitzky-Golay: - Peaks and valleys in the data are meaningful - You want smoothing without losing local structure - Data is relatively smooth (not too noisy)

LOESS: Locally Adaptive Smoothing

LOESS (LOcally Estimated Scatterplot Smoothing) fits local weighted regressions. It’s very flexible and adapts to local data patterns.

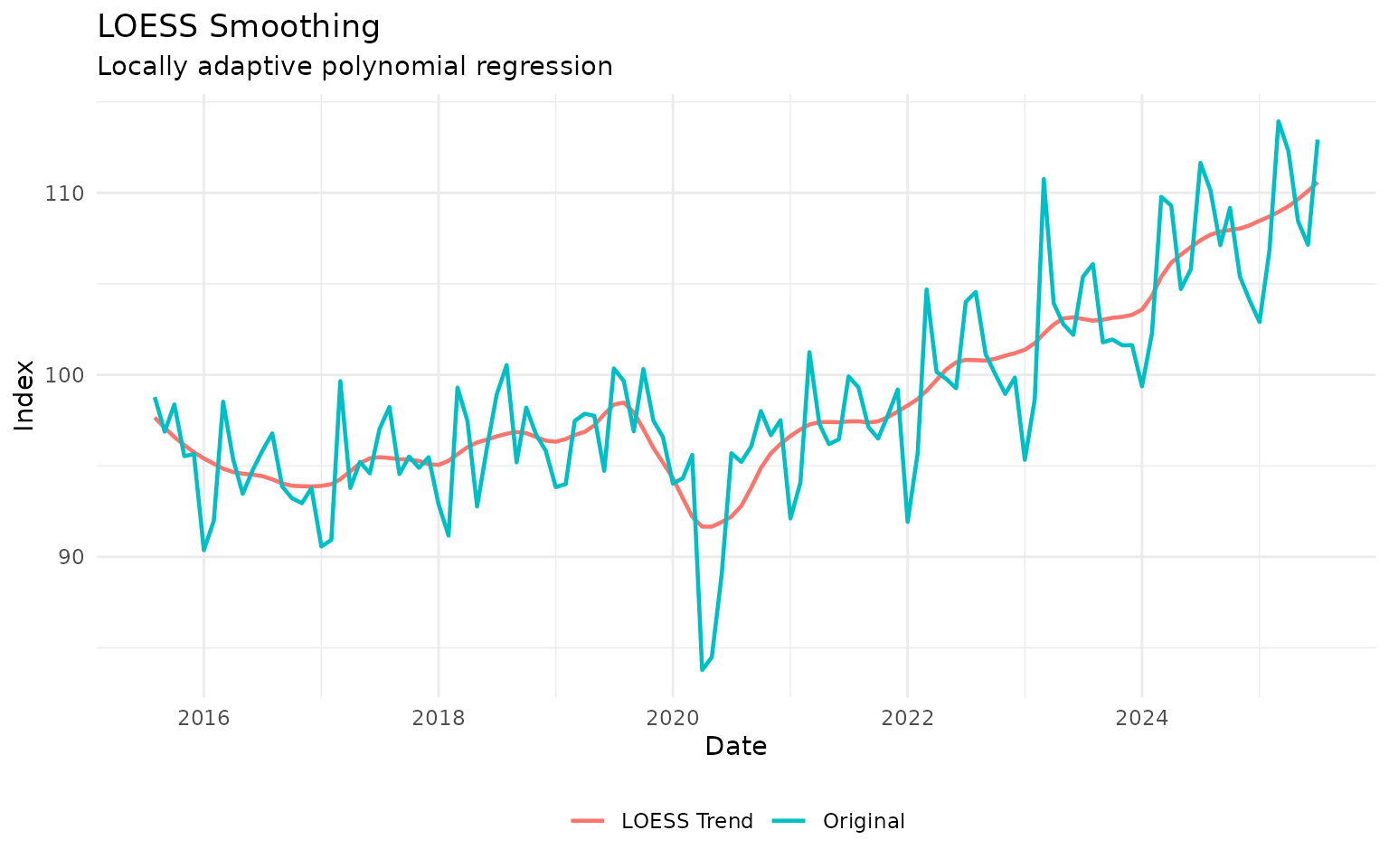

Basic LOESS

# Apply LOESS to IBC-Br

ibcbr_loess <- ibcbr_recent |>

augment_trends(

value_col = "ibcbr",

methods = "loess",

smoothing = 0.2 # Span parameter (0-1)

)

# Plot

ibcbr_loess |>

select(date, ibcbr, trend_loess) |>

pivot_longer(cols = c(ibcbr, trend_loess), names_to = "series") |>

mutate(series = ifelse(series == "ibcbr", "Original", "LOESS Trend")) |>

ggplot(aes(x = date, y = value, color = series)) +

geom_line(linewidth = 0.8) +

labs(

title = "LOESS Smoothing",

subtitle = "Locally adaptive polynomial regression",

x = "Date",

y = "Index",

color = NULL

) +

theme_minimal() +

theme(legend.position = "bottom")

Adjusting the Span Parameter

The span parameter controls smoothness (0-1, where larger = smoother):

# Try different spans

spans <- c(0.1, 0.2, 0.4, 0.7)

ibcbr_spans <- ibcbr_recent

for (span in spans) {

temp <- ibcbr_recent |>

augment_trends(value_col = "ibcbr", methods = "loess", smoothing = span) |>

select(trend_loess)

names(temp) <- paste0("loess_", span)

ibcbr_spans <- bind_cols(ibcbr_spans, temp)

}

# Plot

ibcbr_spans |>

select(date, ibcbr, starts_with("loess_")) |>

pivot_longer(

cols = c(ibcbr, starts_with("loess_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "ibcbr" ~ "Original",

method == "loess_0.1" ~ "Span = 0.1 (flexible)",

method == "loess_0.2" ~ "Span = 0.2",

method == "loess_0.4" ~ "Span = 0.4",

method == "loess_0.7" ~ "Span = 0.7 (smooth)"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "LOESS with Different Span Parameters",

subtitle = "Larger span = smoother trend",

x = "Date",

y = "Index",

color = NULL

) +

theme_minimal() +

theme(legend.position = "bottom")

Recommended span values: - Flexible trend: 0.1 - 0.2 - Balanced: 0.2 - 0.4 - Smooth: 0.5 - 0.75

When to use LOESS: - Trend is nonlinear and complex - You want data-adaptive smoothing - Sample size is moderate (LOESS can be slow on very large datasets)

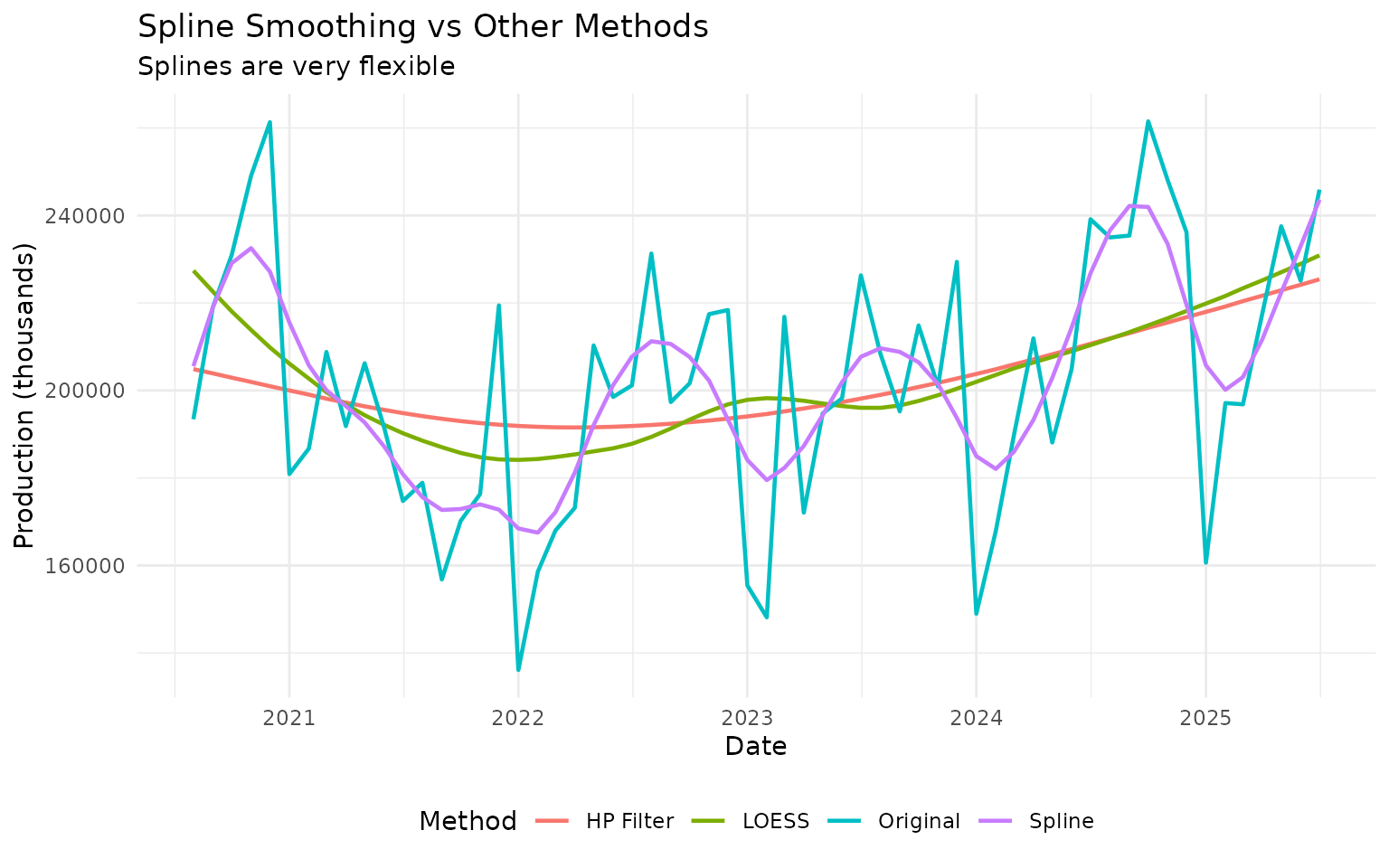

Spline Smoothing: Maximum Flexibility

Splines provide very flexible smoothing by fitting piecewise polynomials:

# Apply spline smoothing

vehicles_spline <- vehicles_recent |>

augment_trends(

value_col = "vehicles",

methods = c("spline", "loess", "hp")

)

# Plot

vehicles_spline |>

select(date, vehicles, starts_with("trend_")) |>

pivot_longer(

cols = c(vehicles, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

mutate(

method = case_when(

method == "vehicles" ~ "Original",

method == "trend_spline" ~ "Spline",

method == "trend_loess" ~ "LOESS",

method == "trend_hp" ~ "HP Filter"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.8) +

labs(

title = "Spline Smoothing vs Other Methods",

subtitle = "Splines are very flexible",

x = "Date",

y = "Production (thousands)",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

When to use splines: - You need maximum flexibility - Trend has complex, changing curvature - You don’t need to explain the method (it’s somewhat of a “black box”)

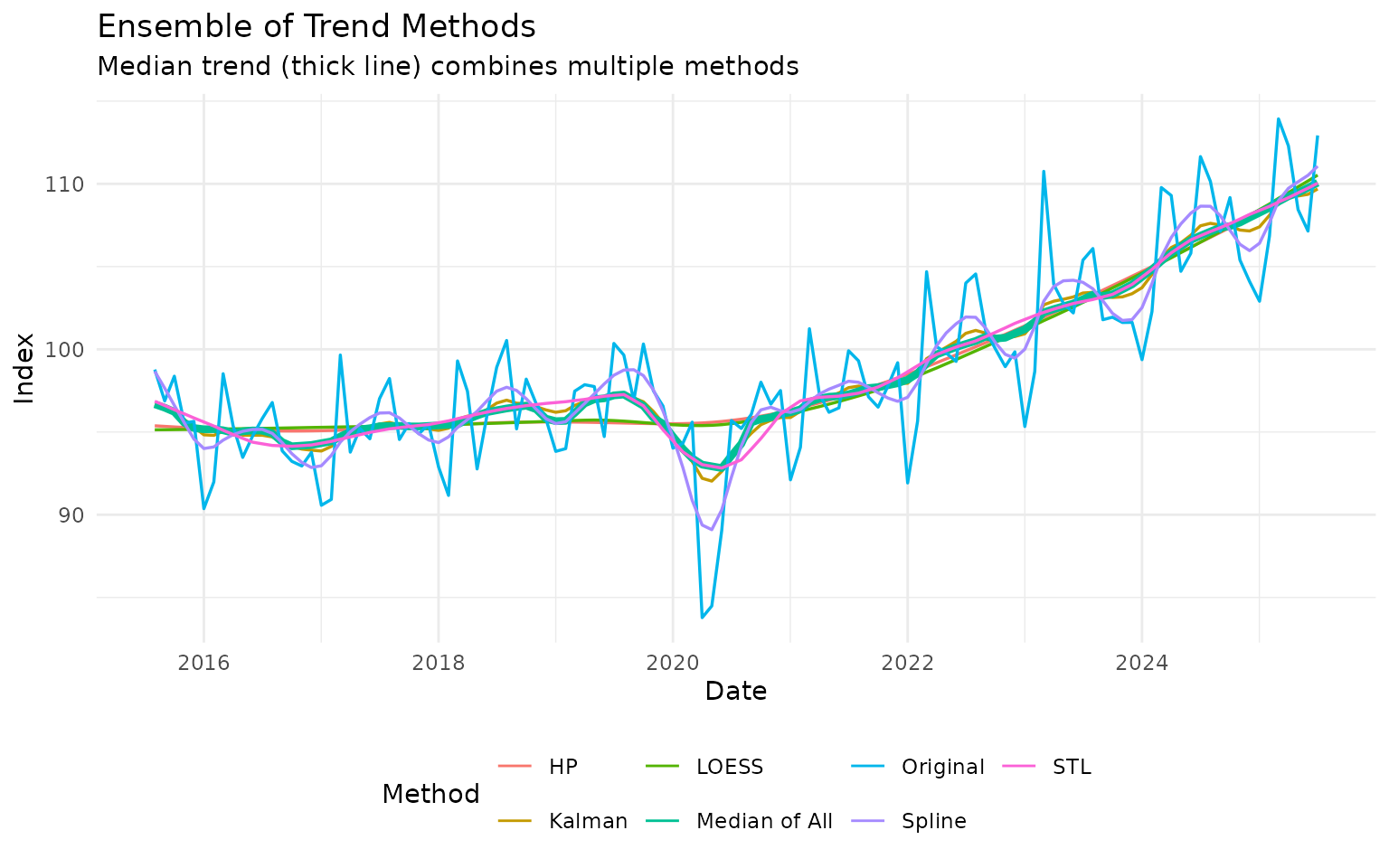

Combining Multiple Methods

Often the best approach is to compare several methods:

# Apply many methods to the same data

multi_method <- ibcbr_recent |>

augment_trends(

value_col = "ibcbr",

methods = c("hp", "stl", "kalman", "loess", "spline")

)

# Calculate median trend across methods

multi_method <- multi_method |>

rowwise() |>

mutate(

trend_median = median(c(trend_hp, trend_stl, trend_kalman,

trend_loess, trend_spline), na.rm = TRUE)

) |>

ungroup()

# Plot

multi_method |>

select(date, ibcbr, starts_with("trend_")) |>

pivot_longer(

cols = c(ibcbr, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

filter(!is.na(value)) |>

mutate(

method = case_when(

method == "ibcbr" ~ "Original",

method == "trend_hp" ~ "HP",

method == "trend_stl" ~ "STL",

method == "trend_kalman" ~ "Kalman",

method == "trend_loess" ~ "LOESS",

method == "trend_spline" ~ "Spline",

method == "trend_median" ~ "Median of All"

),

is_median = method == "Median of All"

) |>

ggplot(aes(x = date, y = value, color = method, linewidth = is_median)) +

geom_line() +

scale_linewidth_manual(values = c(0.6, 1.5), guide = "none") +

labs(

title = "Ensemble of Trend Methods",

subtitle = "Median trend (thick line) combines multiple methods",

x = "Date",

y = "Index",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

The median trend can be more robust than any single method.

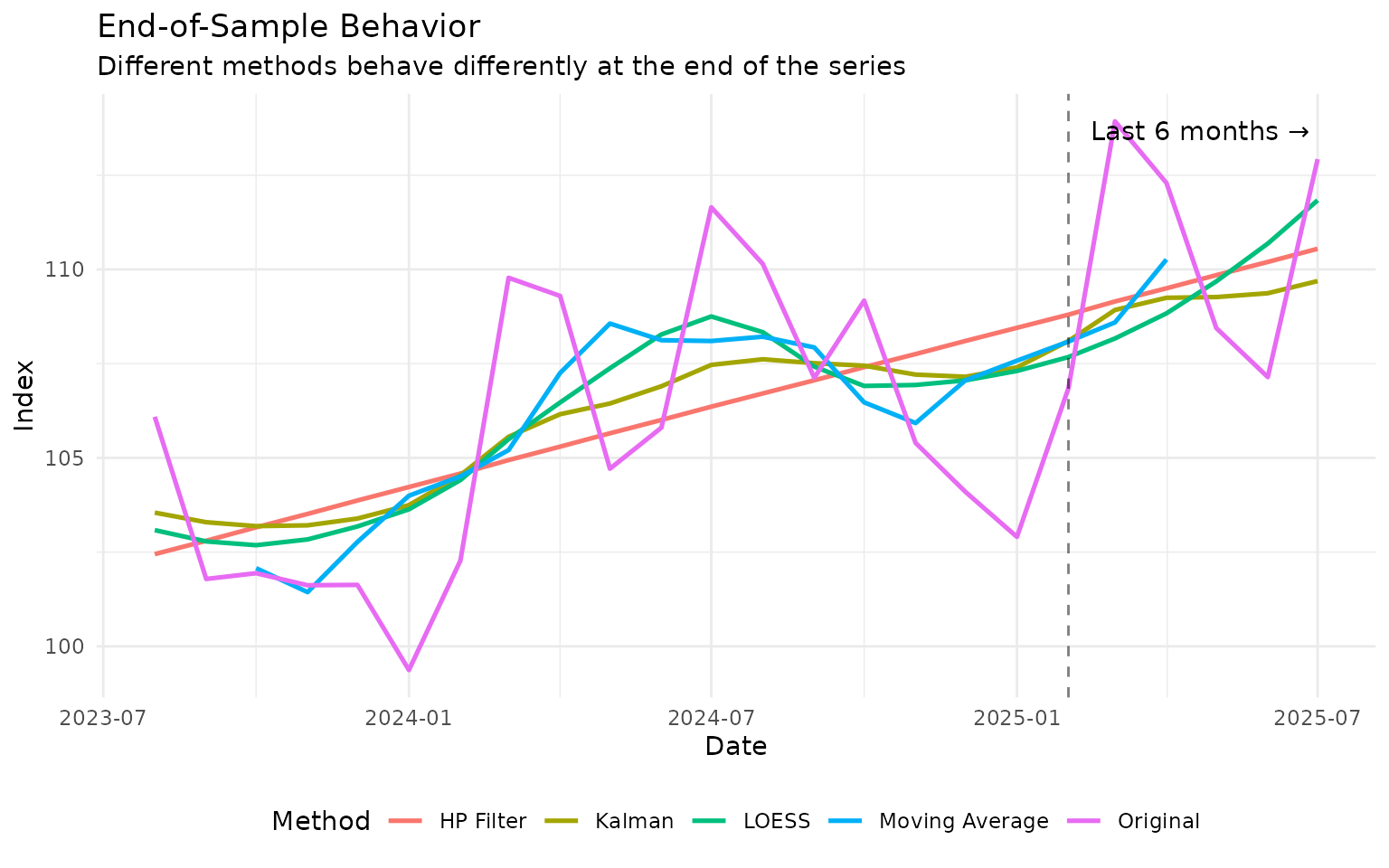

Practical Application: End-of-Sample Problem

A common issue with trend extraction is behavior at the end of the sample (most recent data). Different methods handle this differently:

# Focus on the last year of data

recent_12m <- ibcbr |>

slice_tail(n = 24)

# Apply multiple methods

end_sample <- recent_12m |>

augment_trends(

value_col = "ibcbr",

methods = c("hp", "kalman", "loess", "ma"),

window = 6

)

# Highlight the last 6 observations

end_sample <- end_sample |>

mutate(recent = row_number() > 18)

# Plot with emphasis on recent period

end_sample |>

select(date, ibcbr, starts_with("trend_"), recent) |>

pivot_longer(

cols = c(ibcbr, starts_with("trend_")),

names_to = "method",

values_to = "value"

) |>

filter(!is.na(value)) |>

mutate(

method = case_when(

method == "ibcbr" ~ "Original",

method == "trend_hp" ~ "HP Filter",

method == "trend_kalman" ~ "Kalman",

method == "trend_loess" ~ "LOESS",

method == "trend_ma" ~ "Moving Average"

)

) |>

ggplot(aes(x = date, y = value, color = method)) +

geom_line(linewidth = 0.9) +

geom_vline(xintercept = end_sample$date[19], linetype = "dashed", alpha = 0.5) +

annotate("text", x = end_sample$date[19], y = max(end_sample$ibcbr, na.rm = TRUE),

label = "Last 6 months →", hjust = -0.1, vjust = 1) +

labs(

title = "End-of-Sample Behavior",

subtitle = "Different methods behave differently at the end of the series",

x = "Date",

y = "Index",

color = "Method"

) +

theme_minimal() +

theme(legend.position = "bottom")

Key insights: - MA has NAs at the end (needs future data) - HP, Kalman, and LOESS all provide estimates at the end - Kalman filter often handles the end-of-sample best

Method Selection Guide

Decision Tree

-

Does your data have seasonality?

- Yes → Use STL

- No → Continue to step 2

-

Do you need to preserve peaks/valleys?

- Yes → Use Savitzky-Golay or LOESS

- No → Continue to step 3

-

Is this for business cycle analysis?

- Yes → Use HP filter (see economic-filters vignette)

- No → Continue to step 4

-

Do you need maximum flexibility?

- Yes → Use LOESS or Spline

- No → Continue to step 5

-

Do you want statistically optimal smoothing?

- Yes → Use Kalman filter

- No → Use Moving Average or HP filter

Method Summary Table

| Method | Seasonality | Peaks | Flexibility | Speed | Complexity |

|---|---|---|---|---|---|

| STL | ✓ | Medium | Medium | Fast | Low |

| Kalman | - | Medium | Medium | Fast | Medium |

| Savitzky-Golay | - | ✓ | High | Fast | Medium |

| LOESS | - | ✓ | High | Slow | Low |

| Spline | - | Medium | Very High | Fast | High |

Parameter Quick Reference

STL:

# Default works well for most seasonal data

data |> augment_trends(value_col = "value", methods = "stl")

# Adjust window for seasonal component

data |> augment_trends(

value_col = "value",

methods = "stl",

window = 13 # Must be odd

)Kalman:

# Light smoothing

data |> augment_trends(value_col = "value", methods = "kalman", smoothing = 0.5)

# Heavy smoothing

data |> augment_trends(value_col = "value", methods = "kalman", smoothing = 5.0)Savitzky-Golay:

# Standard setup

data |> augment_trends(

value_col = "value",

methods = "sg",

window = 9, # Must be odd

params = list(sg_poly_order = 3)

)LOESS:

# Flexible (less smooth)

data |> augment_trends(value_col = "value", methods = "loess", smoothing = 0.15)

# Balanced

data |> augment_trends(value_col = "value", methods = "loess", smoothing = 0.3)

# Smooth

data |> augment_trends(value_col = "value", methods = "loess", smoothing = 0.6)Spline:

# Default usually works well

data |> augment_trends(value_col = "value", methods = "spline")Common Pitfalls

Pitfall 1: Using STL on Non-Seasonal Data

Problem: STL fails or gives weird results Solution: Check if data actually has seasonality. Use ACF plot or visual inspection.

Pitfall 2: LOESS Too Flexible

Problem: Trend tracks data too closely, includes noise Solution: Increase span parameter (try 0.3-0.5 instead of 0.1-0.2)

Summary

Advanced methods provide powerful alternatives to standard approaches:

- STL: The go-to method for seasonal data

- Kalman: Statistically optimal, great for real-time filtering

- Savitzky-Golay: Preserves local features better than MA

- LOESS: Flexible, data-adaptive smoothing

- Spline: Maximum flexibility when you need it

Best practices: - Start simple (MA or HP) before trying advanced methods - Compare multiple methods to ensure robustness - Visualize results - don’t just trust the numbers - Consider the trade-off between smoothness and responsiveness

Further Reading

- For basic methods: See “Getting Started” vignette

- For moving averages: See “Moving Averages” vignette

- For business cycles: See “Economic Filters” vignette

- For STL details:

?stats::stl - For Kalman filtering:

?dlm::dlmSmooth

References

- Cleveland, R. B., Cleveland, W. S., McRae, J. E., & Terpenning, I. (1990). STL: A seasonal-trend decomposition. Journal of Official Statistics, 6(1), 3-73.

- Kalman, R. E. (1960). A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1), 35-45.

- Cleveland, W. S. (1979). Robust locally weighted regression and smoothing scatterplots. Journal of the American Statistical Association, 74(368), 829-836.

- Savitzky, A., & Golay, M. J. (1964). Smoothing and differentiation of data by simplified least squares procedures. Analytical Chemistry, 36(8), 1627-1639.